- Dissertation Topics (185)

- Accounting Dissertation Topics (8)

- Banking & Finance Dissertation Topics (10)

- Business Management Dissertation Topics (35)

- Economic Dissertation Topics (1)

- Education Dissertation Topics (12)

- Engineering Dissertation Topics (9)

- English Literature Dissertation Topics (3)

- HRM Dissertation Topics (3)

- Law Dissertation Topics (13)

- Marketing Dissertation Topics (9)

- Medical Dissertation Topics (7)

- Nursing Dissertation Topics (10)

- Other Topics (10)

- Supply Chain Dissertation Topics (2)

- Research Topics (16)

- Biomedical Science (1)

- Business Management Research Topics (1)

- Computer Science Research Topics (1)

- Criminology Research Topics (1)

- Economics Research Topics (1)

- Google Scholar Research Topics (1)

- HR Research Topics (1)

- Law Research Topics (1)

- Management Research Topics (1)

- Marketing Research Topics (1)

- MBA Research Topics (1)

- Medical Research Topics (1)

- Guide (63)

- How To (32)

- List (20)

Table of Contents

CHAPTER 4: FINDINGS AND DISCUSSION

Introduction

Stock returns and volatility are the two main factors that influence the behaviour of investors and shareholders and this behaviour is critical to study for any researcher as they need higher returns and minimum possible risk and volatility with their investments. But literature suggests that equity multiple can strongly influence these two factors. It is a special type of financial metric that compares the cash amount being invested and generated from that investment over a specific time period. Similarly the stock returns are the amount being generated or received by the shareholders by the purchase of stock. Divedents are not the only form of stock returns but capital appreciation also falls in the same category as suggested by Easley and O’hara in 2010.

Besides, the volatility in stock also vaies the price of stock of any company. Many factors including economic, political or even rumors can be the cause for either the decline or increase in the stock price. Therefore, equity multiples, stock volatility and stock returns are the main focused factors of the study. The goal of the following chapter is to provide the results and discuss those findings in order to achieve the objectives of the study. The main aim of the study is to determine the impact of equity multiples on stock returns and volatility. Therefore, for covering the aim and objectives, the study had been conducted through analysing the financial data of 10 listed Pakistani companies for reaching to a conclusion that the equity multiples impacts on the stock returns and volatility on the Pakistani companies. The elements that had been covered in the following chapter are descriptive statistics, correlation analysis, and panel data regression analysis of the gathered data. Lastly, the objectives had also been discussed while relating to the findings of the study along with the chapter summary.

Descriptive Statistics

In an attempt to understand the general nature of the data relating to central propensity, minimum and extreme of the data, the researcher has used descriptive analysis. For that purpose mean, extreme, standard deviation and minimum have been calculated using E-Views software. The most common method used for measuring the central propensity of the data is through mean statistics. The mean value that is calculated from the descriptive statistics is the average value of all the samples that are involved in the study. For determining the mean value, the common technique is to compute the total value of the factors and then finally divide by the total numbers of the value. The other factor that had been analysed in the descriptive statistics is the maximum value in highest value in the sample had been obtained for identifying the largest value. Similar, to the maximum value, the minimum value had also been calculated by determining the smallest value on the samples. The median value that is obtained through descriptive statistics is the middle value on the data set of the variables and is identified in the centre of the variable. Lastly, the standard deviation had been analysed on the descriptive statistics which provides with the most detailed and reliable description on the dispersion. According to the study of Bickel and Lehmann (2012) the term dispersion denotes the distance between the mean and quantity. A lower value of standard deviation suggests that the data inclines to be closer to the mean value of data set whereas a higher value indicates that the data are highly spread out on the average value of the data set.

According to the study of Erlingsson and Brysiewicz (2013) the descriptive statistics is highly important for the researchers and analysts as it presents the data which is easily visualized. It is an effective method for transforming the raw data into meaningful information that can be easily understood by the analyst and the researcher. Moreover, the study had highlighted that the descriptive statitics helps in providing with basic information regarding the variables in the data set and also highlighting the association among the variables. The generated results can be viewed in the tabular format as follows:

In accordance with the table, the variable of equity multiple has an average value of 22.45 where as the median is relatively lesser which is 10.09. Besides, the maximum value is obtained to be 958.17 and minimum is 1.58. In this concern, the standard deviation is computed to be quite high.

The variable of firm performance has a mean value of 23.92% which is the net margin while the median value is also relatively lower which can be seen as 7.74%. In addition, the maximum value if 658.49% while the minimum value is computed to be negative and is 18.96%. Besides, the standard deviation is also high which is asserting that amongst the companies, the differences in the net margins are quite high.

Industry growth is another variable which can be deemed as control variable and in this concern, the mean value is 1% over the span of 10 years with median value of 4%. Besides, maximum value is reached to be 6% and the minimum value is computed to be negative (-15%).

The variability in the data is quite high as the value is 6%.

Stock return is one of the dependent variables of the study which has an average of 20% with the median is of 13%. The supreme return is computed to be 187% with minimum of -89%. Given this, the standard deviation is computed to be 49%.

The last variable or another reliant variable is stock volatility whose mean is computed as 24% whilst the median value is 9%. Moreover, the maximum volatility can be seen as 230% with minimum value of 0%, however, this implies higher deviation of 37%.

Correlation Analysis

The statistical technique which is the correlation analysis had been used for measuring the relationship between the identified variables. The correlation is mainly used for defining the power, type and significance of the. The table below shows the results of the correlation analysis based on the data gathered:

The above table denotes the results of the correlation analysis in which the Pearson correlation had been utilized. The values on the table represent the coefficient in which it is less than 0.5 and does not have a negative sign is a weak and positive relationship and the coefficient between 0.5 and 0.7 is said to have a positive moderate relationship. Moreover, the coefficient which is higher than 0.7 is said to have a strong and positive relation; however, coefficients which negative sign would indicate a negative relationship.

From table 2, it can be noted that there are mainly five variables in the correlations analysis which consist of stock volatility, stock return, industry growth, firm performance and equity multiples. When analysing the variable stock volatility, it had coefficients of -0.02, 0.04 and 0.015 with the equity multiple, firm performance and industry growth, respectively. This shows a weak relationship; however, stock volatility had a negative relationship with equity multiple due to having -0.02 coefficient and has positive association with others. Pertaining to the significance of the relationships then it is found between stock volatility and industry growth. Moving on to stock return, it had a coefficient of -0.048, 0.065 and 0.12 with equity multiple, firm performance and industry growth, respectively. Hence, the significance is found only with the industry growth. The significance has been asserted on the basis of p-value because if it is computed to be less than 5% then the relationship is deemed significant. This further indicates a weak positive relationship with the two variables; however, the stock yield had a coefficient of –

0.048 with equity multiples which had indicated a negative relationship.

Based on the above analysis, it can be specified that stock volatility had a weak positive relationship with the stock return, industry growth and firm performance whereas have a negative relationship with the equity multiples. Where as, the stock return had a weak positive relationship with industry growth, financial presentation and stock volatility whereas had a negative relationship with equity multiples. However, not all relationships can be deemed as significant.

Panel Data Regression Analysis

Another statistical tool used for evaluating and measuring the impact of the variable is the panel data regression analysis. The data accumulated pertaining to the variables of firm performance, industry growth, stock returns, stock volatility, and equity multiples have been computed of 46 companies listed in PSX while the data ranged from 2009 to 2018. This asserts that cumulatively, the data forms a panel based on cross-section of companies and period ranging from 2009 to 2018. The regression analysis is used for determining the influence of the independent variable on the dependent variable. The dependent variables that had been identified in this study are a stock return and stock volatility. The independent variable is the industry growth, firm performance and equity multiples. Since there are two dependent variables determined in the study; therefore, panel least squares have been computed twice with stock volatility as first dependent variable and stock returns as second dependent variable. Given this, the data have been assessed for fixed and random effect models as to which one can be deemed as more appropriate model and to clarify the most appropriate model, Hausman testing has been done. The underlying reason for choosing fixed or random model is associated with the reality because pooled OLS usually ignores the panel or specific effects associated with the crosssections or time variances and to cater to such problem the latter is not employed.

The two regression model that had been applied on the two dependent variables, volatility and return of stock are the fixed effect model and random effect model. The fixed effect model is that type of regression model where it is expected that the independent variables are static and the dependent variables are changed besed on the level of independent variables. In general, this particular statistical model treats all variables of the study as non-random values. For instance, the variables such as age, ethnicity and sex does not change; therefore, these variable are fixed over time and the fixed effect model is suitable in these kind of variables.

On the contrary, the opposite of fixed effect model is the random effect model which is also used in measuring the stock volatility and stock return. The statistical model random effect is that particular model that represents the factors on random effects. The random effect model are also considered as hierarchical model. This implies that all the variables of the study are treated as random values. There are various situations where it is required to predict and analyst the response through the random effect. Moreover, the random effect had been considered to have normal distribution where the value of mean is zero. Below are the results of random and fixed effect models that had been calculated for the stock returns and stock volatility along with its interpretation.

Stock Returns

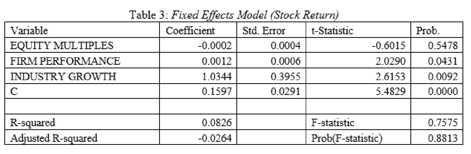

The results pertaining to fixed effects model can be viewed as follows where the dependent variable is considered to be stock returns:

As per the table provided above, the model represents the results of the fixed effect PLS regression in which the dependent variable that had been considered is the stock return. From the above table, the R-squared is 0.0826 or 8.26% which indicates that the dependent variable is explained and interpreted by 8.26% through the independent variables’ variance. Other than that, the firm performance and equity multiples have the significance values more than 0.05 which indicates that all the independent variable does not influence the stock return. Besides, the variable of industry growth is found to have significance value of 0.009 which is below 5%. Therefore, the result is found to be important while coefficient is positive as the sign with 1.03 is positive. It shows that the impact that industry growth has on stock returns is positive which means that stock returns are dependent on the industrial patterns. Moreover, the overall regression is computed to be insignificant because, p-value of f-statistics is computed to be 0.88. In addition, since the data is panel therefore, the researcher has also computed random effects model while undertaking the same variables. The results of random effect model with the dependent variable stock return can be seen as follows:

In the perspective of the random effect model, the variables of equity multiples and firm performance are computed to be insignificant. It has been asserted because the p-values are above the threshold of 5%. Given this, the variable of industrial growth is significant as the pvalue is 0.009. Moreover, the effect is found to be positive which can be interpreted as increment in industrial growth will lead to positive and incremental returns. Alternatively, the R-square value is computed to be 2.3% which can be translated as- variance in independent variables that are equity multiples, firm’s performance and industry growth is cumulatively explaining only 2.3% variation in the stock returns. Besides, the overall model is totaled to be major as the pvalue is 0.01 which is below 5%. However, to decide whether fixed effect is better or random effects model, the hausman test has been performed. The results have been displayed as follows while the null hypothesis is that the random model is better:

In accordance with the statistics of hausman tests, the chi square statistics that had been obtained from the test is 3.597 and also highlight the degree of freedom in the above table. Moreover, the probability value had been identified as 0.304 in which the null hypothesis cannot be invalid which infers that random effect model is better in this case. The reason that the null hypotheis had been negated as the value 0.304 is higher than 5% (0.05) .Hence, the effects of fixed effect model are not much relevant in comparison with the random effect model. However, in cumulative manner, it can be inferred that the influence of equity multiples on the stock returns of PSX listed companies is not found to be significant in any manner therefore, the effect is negated. Overall, by conducting the hausman test it had been found that the random effect model has been found much effective matched to the random effect model in the stock returns.

Stock Volatility

Another dependent variable is the volatility of stock market while the independent variables are same that are equity multiples, firm’s performance and industry growth. Firstly, fixed effect model has been computed while the results can be viewed as follows:

The table presented above represents another result of the regression analysis pertaining to fixed effects in which the dependent variable which time had been considered is the stock volatility. Built on the results of the table, the R-square is 33.93% which indicates that the dependent variable is explained and interpreted by 33.93% through the independent variables that are equity multiples, firm’s performance and industry growth. Besides, the adjusted Rsquared is reduced to 26.08% with the inclusion of excessive variables in the model. Other than that, the firm performance and equity multiples have the significance values more than 0.05 which indicates that all the independent variable does not influence the stock volatility of the companies listed on PSX. Besides, the variable of industry growth is found to have significance value of 0.0001 which is below 5%. Therefore, the result is found to be noteworthy while coefficient is positive as the sign with 1.03 is positive. It shows that the impact that industry growth has on stock returns is positive which means that stock returns are dependent on the industrial patterns. Moreover, the overall regression is computed to be important because, pvalue of f-statistics is computed to be 0.000. In addition, since the data is panel therefore, the researcher has also computed random effects model while undertaking the same variables. The results of random effect model with stock returns as dependent variable can be seen as follows:

In case of random effect model, the variables of equity multiples and firm performance are computed to be insignificant which is the same case as woth the fixed effect model. It has been deduced because the p-values are above the threshold of 5%. Given this, the variable of industrial growth is important as the p-value is 0.000. Moreover, the effect is found to be positive which can be interpreted as increment in industrial growth will lead to positive and incremental instability in the stocks of PSX listed companies. On the other hand, the R-squared value is computed to be 3.7% which can be translated as- variance in independent variables that are equity multiples, firm’s performance and industry growth is cumulatively explaining only 3.7% variation in the stock volatility. Besides, the overall model is computed to be important as the pvalue is 0.001 which is below 5%. However, to decide whether fixed effect is better or random effects model, the hausman test has been performed. The results have been displayed as follows while the null hypothesis is that the random model is better:

In accordance with the statistics of hausman tests which is 0.22 with p-value of 0.97, the null hypothesis cannot be negated which infers that random effect model is better in this case. Moreover, the probability value being above 5% which is 0.9737 specifies that the null hypothesis cannot be negated. Hence, the results of fixed effect model are not much relevant in comparison with the random effect model. It states that all undertaken companies have a mean intercept. Cumulatively, it can be inferred that the result of equity multiples on the stock volatility of companies listed on PSX is not found to be significant in any manner therefore, the effect is negated. Thus, the effects of the Hausman test shows that the fixed effect model is not much relevant or reliable while comparing it with the random effect model.

Discussion of Objectives

Objective 1: To conceptualize equity multiples, stock returns and volatility.

The first objective of the study that had been formulated by the researcher was to conceptualize the equity multiples, stock returns and volatility. This objective had been successfully achieved through the review of literature which supported the researcher in understanding the concepts. The study of Aroni (2011) had indicated that the term equity multiples consists of various effective financial metrics that is utilized for comparing the investment of the investors for the given period time. The study of Patton and Sheppard (2015) had highlighted that the equity multiplies are generally determined through dividing the received cash with the total equity invested. Moreover, the study had highlighted it is commonly calculated on the commercial estates and properties. If the equity multiple is calculated to be higher than 1 than this shows that the investment made by the investor had been covered and had been further generating profits. On the contrary, if the value of equity multiple is lower than 1, then this indicates that the investor had been receiving less than what had been invested. Furthermore, if the equity multiple is equal to 1, then this shows that the receivable had only covered the investment without generating any additional profits. On the hand, the term stock return as defined by Al-Shurbiri (2010) is the returns that had been received by the shareholders on their purchases of stock. It is the responsibility of the firm in providing positive returns to the shareholders for satisfying them and also attracting potential shareholders. Moreover, the study had highlighted that even if an organization has high return on equity, the shareholders may still suffer due to numerous factors that may reduce the value of the stock. This highlights that the stock returns may not be necessary affected by the profitability of the company but the other factors needs to be also considered such as the market position and expectations of the stock. Other than that, the study of Easley and O’hara (2010) had highlighted that the stock returns maybe in the form of dividends or capital appreciation. Therefore, it is critical for the organizations to providing psotivie returns to the shareholders for not only satisfying their existing investors but also attracting more potential shareholders. Lastly, Ouma and Muriu (2014) had defined stock volatility as the changes in the prices of the stock which can be the result of various internal and external reasons. The stock volatility can also even occur due to a rumour regarding the company that it may face loss in the future which may cause the stock prices to reduce in a significant manner. For instance, if an organization has been facing law suites due to any penalties, it may result in causing the stock prices to decline. Thus, it is highly important for the management of the company for ensuring that there are no rumours in the markets that may affect its operations, internal control and profitability. Moreover, the study of Al-Shubiri (2010) had highlighted that the stock volatility is risky situation for both the shareholders and company as high volatility on the stock price may cause the shareholders to lose their interest on investing in the company to avoid risk. This may cause the company to lose its stakeholders and also causing damage to the reputation of the company. On the basis of the above analysis from the literature, the three factors stock volatility, stock return and equity multiples are highly important to be studies as it is highly associated with the company and the shareholders.

Objective 2: To depict factors affecting stock returns.

The second goal of the study was to determine the issues that affect the stock return. This objective was also theoretical in nature and had been successfully achieved through the review of the literature. The literature had highlighted various issues that disturb the stock returns in which the study of Christensen and Zhu (2010) had indicated that the financial and non-financial performance of a firm has a important effect on the stock returns. The poor performance of the company in its financial aspect would also cause the prices of the shares to decreases. On the other hand, the companies that had been excellently performing in the market are not only able to enhance the share returns but also increases the trust and demand of the stock of the company. Moreover, the study had also highlighted that the shareholders are only involved with the firms that are effectively performing in the market, have high return on equity and have competitive edge. Therefore, the one major factor for influencing on the stock return of the company is the company’s performance. Another factor which affects the return of the stock is the inflation which is a macro environment factor. The term inflation is described as the growth of the products and services prices which as a result affects the stock prices and returns as well. As stated in the study of Easley and O’hara (2010), the higher the inflation of the economy, the lower the stock prices and returns. Thus, the central bank plays an important role by introducing procedures and policies for handling inflation such as through increasing the rate of interest for decreasing the amount of fund. Then again, the increase of interest can cause stock prices to decrease due to having an inverse relationship. Thus, it is critical for the central bank to implement policies and plans that would enable the firm to improve its stock returns which would not intensify the value of the company but also increase the FDI inflows causing favourable conditions for the company as well. Therefore, on the basis of the arguments, both inflation and interest rate has the potential of significantly affecting the stock price of the company.

The third factor to influence on the stock return is the exchange rates which are also considered the major factor for influencing. The outperformance of the stock market of a country can result in causing the current exchange rate to enhance. Moreover, it also has an opposite reaction as defined by Peiro (2016) that the investors who hold the shares are highly exposed to fluctuation due to the volatility in the change rates. Moreover, the study of Peiro (2016) had highlighted that the foreign investors are highly interested towards investing to the countries where the exchange rate is high which may provide opportunity to the shareholders for increasing their return. Therefore, the investments made by the foreign investors may result in increasing the share price of the company. Therefore, it can be indicated that the exchange rate is also an vital factor for the stock returns. As said by Phan and Narayan (2015), the stock market returns are also influenced by crude oil prices. The prices of oil can be considered as a useful predictor for measuring the treads of stock returns. Thus, the upturn or fall in the oil prices can cause an effect to the stock return. The other factors for affecting the prices of stock return were foreign direct investment. As per the study of Nazir and Ahmed (2010), there is a association between the stock market and FDI. High foreign direct investment can overall improve the economic growth of the country that results in causing a positive impact on the stock prices and returns. Similarly, the study had also been conducted by Yan (2011) who had highlighted that the stock growth and FDI has a important positive association. This specifies that the increase of the FDI inflows may result in improving not only the stock returns but also improving the economy of the country which is also beneficial for the listed company of that particular country. Thus, the literature review had provided with mainly 5 factors for influencing on the stock prices which consist of the company’s performance, inflation, exchange rates, prices of crude oil and foreign direct investment.

Objective 3: To assess the relationship between equity multiples, stock returns and risk.

The third objective of the study that had been proposed by the researcher emphases on assessing the connection between the equity multiples, stock returns and risks. This type of research objective is theoretical and qualitative in nature which had been achieved through literature review. The investors consider the potential risks while investing as it is the objective and goal of every investor in generating higher returns while minimizing their losses. Therefore, it is comprehensive for the investors for gathering information regarding the investments by analysing the indicators that may have the influence towards the stock returns. Similarly, the study of Aroni (2011) had highlighted that there are three main approaches for determining the value of the firm which consist of discounted cash flow, relative valuation and contingent claim. The most common method that is adopted by the inventors is the relative valuation that helps in the analysing the company. The study of Easley and O’hara (2010) had indicated that the equity multiples, stock return and risks have a positive relationship and are related to one another. Moreover, the study has highlighted that the investors consist of two kinds which are risk averse and risk seekers. The risk-averse investors are those savers who are not eager to take high risk for gaining higher returns whereas the risk seekers are those investors who are willing to take high risks for higher returns.

The study of Patton and Sheppard (2015) had highlighted that risk seekers high assess the risk before investing their money. These risks are commonly measured from the equity multiples which supports in analysing the investment. On the other hand, Fabozzi and Markowitz (2011) had indicated that the positive association between the stock return, risk and equity multiples is not guaranteed when there no efficient market in the country. Furthermore, the study accompanied by Nazir and Ahmed (2010) had emphasized that the equity multiples supports the investors in determining the returns that the investment can generated and also further helps the investor whether he/she should continuing keeping the stock or trades it. The equity multiple is the easiest and simplest metric for analysing an investment that determines the futures of investment. Various studies had been conducted for exploring the relationship among the stock returns, equity multiples and stock multiples; however, the study conducted by Fabozzi and Markowitz (2011) had highlighted that the Pakistan stock market is usually effected by the economic and political situations.

Objective 4: To depict the impact of equity multiples on stock returns and volatility in Pakistan stock exchange.

The last goal of the study was to regulate whether the equity multiples impacts on the stock volatility and stock returns on Pakistani Stock Exchange. This objective was quantitative in nature which is considered as the crucial objective for the study. The data had been gathered from 46 listed Pakistani companies in which the data had been collected from stock volatility, stock return, industry growth, financial performance and equity multiples. According to the study of Aroni (2011), there are various types of equity multiples that is used for the valuation of the company. However, the equity multiples had been considered for the gathering of data is the P/E ratio for the Pakistani registered companies. Once the data had been obtained from the relevant sources such as the Pakistan stock market, Reuters and others, the reliable statistical techniques had been applied which consist of descriptive statistics, correlation analysis and panel data regression analysis. The purpose of the descriptive statistics was to represent the raw data of the variables into a meaningful form that helped in easily analysing their data set. The values that had been represented from the descriptive statistics consist of mean, median, minimum, maximum and standard deviation.

The correlation analysis had also been conducted for measuring the variables association with one another. The consequences gained from the correlation study had specified that both stock volatility and stock return had a weak relationship with the equity multiples. However, both stock volatility and stock return had negative association with equity multiples as the coefficient were negative. Furthermore, the panel data regression analysis had been conducted which consists of fixed and random effect model. The outcome gained from the fixed and random effect model had indicated that the equity multiples does not impact on the stock volatility and stock return due to its important value being more than 0.05. Therefore, the results show that the stock return and stock volatility of 46 listed companies in PSX which represents the overall companies of the stock market had not been affected by the equity multiples. The results of the study match with Fabozzi and Markowitz (2011) in which the positive relationship and impact are not guaranteed between the equity multiples, stock return and volatility due to inefficient market. This shows that the stock returns and stock volatility could be affect by different interior and exterior factors. For instance, interior factors consists of the company’s presentation such as its sales, net profits, positive rumours and etc. Other than that, the external factors could be inflation, exchange rates, crude oil prices and foreign direct investment.

Stock return is one of the dependent variables of the study which has an average of 20% with the median is of 13%. The supreme return is computed to be 187% with minimum of -89%. Given this, the standard deviation is computed to be 49%.

The last variable or another reliant variable is stock volatility whose mean is computed as 24% whilst the median value is 9%. Moreover, the maximum volatility can be seen as 230% with minimum value of 0%, however, this implies higher deviation of 37%.

Correlation Analysis

The statistical technique which is the correlation analysis had been used for measuring the relationship between the identified variables. The correlation is mainly used for defining the power, type and significance of the. The table below shows the results of the correlation analysis based on the data gathered:

The above table denotes the results of the correlation analysis in which the Pearson correlation had been utilized. The values on the table represent the coefficient in which it is less than 0.5 and does not have a negative sign is a weak and positive relationship and the coefficient between 0.5 and 0.7 is said to have a positive moderate relationship. Moreover, the coefficient which is the variables such as age, ethnicity and sex does not change; therefore, these variable are fixed over time and the fixed effect model is suitable in these kind of variables.

On the contrary, the opposite of fixed effect model is the random effect model which is also used in measuring the stock volatility and stock return. The statistical model random effect is that particular model that represents the factors on random effects. The random effect model are also considered as hierarchical model. This implies that all the variables of the study are treated as random values. There are various situations where it is required to predict and analyst the response through the random effect. Moreover, the random effect had been considered to have normal distribution where the value of mean is zero. Below are the results of random and fixed effect models that had been calculated for the stock returns and stock volatility along with its interpretation.

Stock Returns

The results pertaining to fixed effects model can be viewed as follows where the dependent variable is considered to be stock returns:

As per the table provided above, the model represents the results of the fixed effect PLS regression in which the dependent variable that had been considered is the stock return. From the above table, the R-squared is 0.0826 or 8.26% which indicates that the dependent variable is explained and interpreted by 8.26% through the independent variables’ variance. Other than that, the firm performance and equity multiples have the significance values more than 0.05 which indicates that all the independent variable does not influence the stock return. Besides, the variable of industry growth is found to have significance value of 0.009 which is below 5%. Therefore, the result is found to be important while coefficient is positive as the sign with 1.03 is positive. It shows that the impact that industry growth has on stock returns is positive which means that stock returns are dependent on the industrial patterns. Moreover, the overall regression is computed to be insignificant because, p-value of f-statistics is computed to be 0.88. In addition, since the data is panel therefore, the researcher has also computed random effects model while undertaking the same variables. The results of random effect model with the dependent variable stock return can be seen as follows:

In the perspective of the random effect model, the variables of equity multiples and firm performance are computed to be insignificant. It has been asserted because the p-values are above the threshold of 5%. Given this, the variable of industrial growth is significant as the pvalue is 0.009. Moreover, the effect is found to be positive which can be interpreted as increment in industrial growth will lead to positive and incremental returns. Alternatively, the R-square value is computed to be 2.3% which can be translated as- variance in independent variables that are equity multiples, firm’s performance and industry growth is cumulatively explaining only 2.3% variation in the stock returns. Besides, the overall model is totaled to be major as the pvalue is 0.01 which is below 5%. However, to decide whether fixed effect is better or random effects model, the hausman test has been performed. The results have been displayed as follows while the null hypothesis is that the random model is better:

In accordance with the statistics of hausman tests, the chi square statistics that had been obtained from the test is 3.597 and also highlight the degree of freedom in the above table. Moreover, the probability value had been identified as 0.304 in which the null hypothesis cannot be invalid which infers that random effect model is better in this case. The reason that the null hypotheis had been negated as the value 0.304 is higher than 5% (0.05) .Hence, the effects of fixed effect model are not much relevant in comparison with the random effect model. However, in cumulative manner, it can be inferred that the influence of equity multiples on the stock returns of PSX listed companies is not found to be significant in any manner therefore, the effect is negated. Overall, by conducting the hausman test it had been found that the random effect model has been found much effective matched to the random effect model in the stock returns.

Stock Volatility

Another dependent variable is the volatility of stock market while the independent variables are same that are equity multiples, firm’s performance and industry growth. Firstly, fixed effect model has been computed while the results can be viewed as follows:

The table presented above represents another result of the regression analysis pertaining to fixed effects in which the dependent variable which time had been considered is the stock volatility. Built on the results of the table, the R-square is 33.93% which indicates that the dependent variable is explained and interpreted by 33.93% through the independent variables that are equity multiples, firm’s performance and industry growth. Besides, the adjusted Rsquared is reduced to 26.08% with the inclusion of excessive variables in the model. Other than that, the firm performance and equity multiples have the significance values more than 0.05 which indicates that all the independent variable does not influence the stock volatility of the companies listed on PSX. Besides, the variable of industry growth is found to have significance value of 0.0001 which is below 5%. Therefore, the result is found to be noteworthy while coefficient is positive as the sign with 1.03 is positive. It shows that the impact that industry growth has on stock returns is positive which means that stock returns are dependent on the industrial patterns. Moreover, the overall regression is computed to be important because, pvalue of f-statistics is computed to be 0.000. In addition, since the data is panel therefore, the researcher has also computed random effects model while undertaking the same variables. The results of random effect model with stock returns as dependent variable can be seen as follows:

In case of random effect model, the variables of equity multiples and firm performance are computed to be insignificant which is the same case as woth the fixed effect model. It has been deduced because the p-values are above the threshold of 5%. Given this, the variable of industrial growth is important as the p-value is 0.000. Moreover, the effect is found to be positive which can be interpreted as increment in industrial growth will lead to positive and incremental instability in the stocks of PSX listed companies. On the other hand, the R-squared value is computed to be 3.7% which can be translated as- variance in independent variables that are equity multiples, firm’s performance and industry growth is cumulatively explaining only 3.7% variation in the stock volatility. Besides, the overall model is computed to be important as the pvalue is 0.001 which is below 5%. However, to decide whether fixed effect is better or random effects model, the hausman test has been performed. The results have been displayed as follows while the null hypothesis is that the random model is better:

View More Samples

WhatsApp Now

Get Instant 50% Discount on Live Chat!

WhatsApp Now

Get Instant 50% Discount on Live Chat!