- Dissertation Topics (185)

- Accounting Dissertation Topics (8)

- Banking & Finance Dissertation Topics (10)

- Business Management Dissertation Topics (35)

- Economic Dissertation Topics (1)

- Education Dissertation Topics (12)

- Engineering Dissertation Topics (9)

- English Literature Dissertation Topics (3)

- HRM Dissertation Topics (3)

- Law Dissertation Topics (13)

- Marketing Dissertation Topics (9)

- Medical Dissertation Topics (7)

- Nursing Dissertation Topics (10)

- Other Topics (10)

- Supply Chain Dissertation Topics (2)

- Research Topics (16)

- Biomedical Science (1)

- Business Management Research Topics (1)

- Computer Science Research Topics (1)

- Criminology Research Topics (1)

- Economics Research Topics (1)

- Google Scholar Research Topics (1)

- HR Research Topics (1)

- Law Research Topics (1)

- Management Research Topics (1)

- Marketing Research Topics (1)

- MBA Research Topics (1)

- Medical Research Topics (1)

- Guide (63)

- How To (32)

- List (20)

Table of Contents

CHAPTER 4: DATA ANALYSIS AND DISCUSSION

Introduction

The financial performance of the companies is subject to various external forces beside the internal related to the firm. Meanwhile, macroeconomic factors also influence the how firms operate into an economy and its capability to make profit from the operations. Therefore, in order to analyses at what extent the macroeconomic indicators of the Pakistan have been affecting the automobile industry of Pakistan; following chapter is devoted to analyses and address the research questions and achieve aim of the study. Meanwhile, chapter is divided into the four sections; where in firsts section descriptive statistics has been performed including the graphical representation to analyses the characteristics of the data, and observe the patterns. Furthermore, the correlation and regression analysis have been performed to address the primary research questions. In last section, detailed discussion is conducted based on the primary findings of the study, and summary of the chapter is also provided to give reader a comprehensive view of the chapter.

Descriptive Analysis

Following study total 11 companies from automobile sector of Pakistan were selected for 10 years from 2009 to 2018, and these companies include; Al-Ghazi Tractors LTD,

Atlas Honda LTD, Ghandhara Industries LTD, Ghani Automobile Industries LTD,

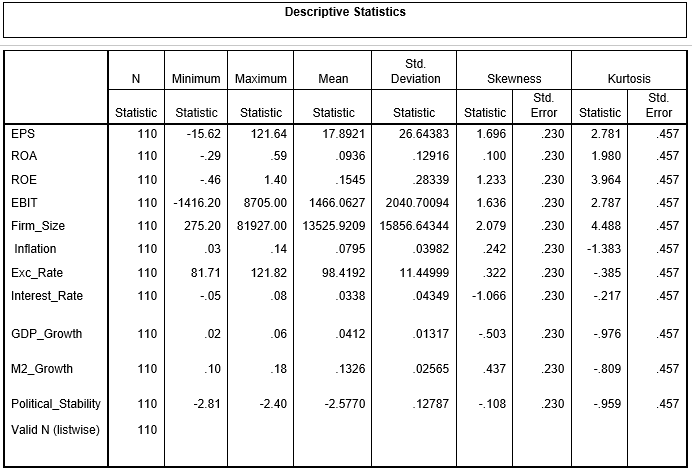

HinoPak Motors LTD, Honda Atlas Cars LTD, Indus Motor Company LTD, Millat Tractors LTD, Pak Suzuki Motors LTD, Sazgar Engineering Works. Meanwhile, following table is presented over give brief description of the data.

The mean EPS of a given company is 17.89 with standard deviation of 24.64 which is higher and implies that there is a significantly difference between the EPS of the selected companies. The minimum and maximum EPS was observed as -15.62 and 121.64 within the companies, and the mean ROA and ROE are 9.36% and 15.45% with standard deviation of 12.91% and 28.33%. Similar to the EPS, the standard deviations of the ROA and ROE are higher implying higher fluctuations into the ROA and ROE of the selected companies. Moreover, the mean EBIT is 1466.06 million with standard deviation of 2040.70 which is also higher than mean value, and minimum EBIT was 1416.20 million and maximum EBIT was 8705 within the data. Furthermore, the mean firm size in terms of total assets is 13525.92 million and has standard deviation of 15856.64 million; where minimum and maximum firm size was 275.20 and 81927 million. This also increases a significant difference between the firm sizes within the selected companies.

Furthermore, the mean inflation in Pakistan is 7.95% with standard deviation of 3.98%, and minimum inflation during the period was 3%, and maximum inflation during period was 14%. This indicates that inflation can rise to as high 14% and increase the costs of doing business. On the other hand, the exchange rate also tends to be affected by the macroeconomic conditions of the country due to the demand and supply of the rupees in international market. Meanwhile, the interest rate, and GDP growth rate mean is 3.38% and 4.12% with standard deviation of 4.34% and 1.31% by which the interest rate and GDP might deviate. And referring to the M2 growth then mean growth rate of M2 is 13.26% with standard deviation of 2.56% by which the money supply might increase or decrease. Furthermore, the political stability of the Pakistan has always been concern for the business community; where as per the World Bank’s indicator of political stability Pakistan’s mean score is at -2.577 which mean Pakistan has weak

political stability.

Therefore, it can be determined that situation of the Pakistan tend to affect the business any time as per the data; and to better understand how variations occurs between the macroeconomic indicators following graph is presented

The graph illustrates how variations occur into the macroeconomic indicators, and illustrates the behavior of the ROA, and ROE line. Therefore, from the graph above it can be observed that there is positive interrelation of macroeconomic indicators with the ROE and ROA of the company; where ROA has not strong relation at some extent as does ROE has with indicators. It implies that changes into the economic policies such as fiscal polies, and monetary policies influences profitability of the Automobile companies in Pakistan. Hence, it is evident that rising inflation and interest rate also can influence firm profitability where country with stronger economic growth and higher demand of automobiles will not be restricted by certain external factors.

Correlation Analysis

Correlation analysis is a statistical method used to evaluate the relationship between two variables. It shows the strength between two variables and helps in seeking out how much one variable affects other variable. It determines the cause and effect and indicates whether the fluctuations in one variable lead to other variable or not. If correlation is closer to 1, it means that there is strong relationship between two variables or it can be said that the independent variable has higher influence on dependent variable. Correlation could be positive or negative as the positive correlation shows that increment in one variable leads to increment in other variable. However, negative correlation indicates that if one variable increases, other variable goes down.

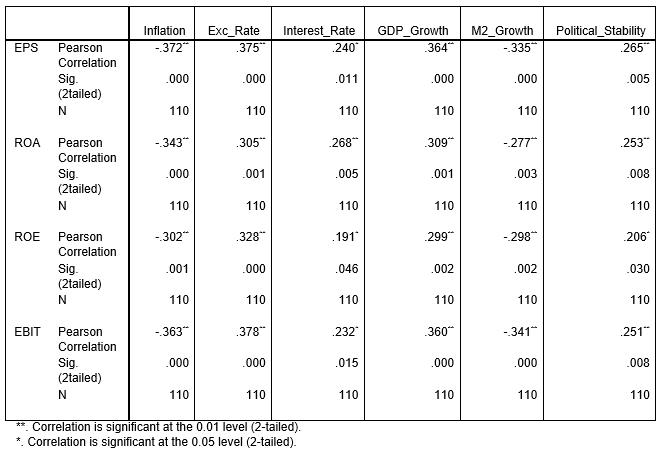

From correlation analysis, it has been observed that the relationship between return on asset and inflation is significant and negative. The sig value between these two variables is 0.00 which is less than 0.05 so it is significant. Meanwhile, the study of Haider et al. (2018) also confirms that return on assets have negative relation with inflation, indicating that higher inflation in the country tend to negatively affect the return on the assets. It means that earnings per share influence the return on asset of Pakistani Automobile Companies. The coefficient value between them is -.343 which shows that they both have negatively related. This result is also supported from the study of Zulfiqar and Din, (2015) who had conducted research on textile companies of Pakistan. He also found that the relationship between ROA and inflation is negative, and this is indicative of the potential interrelation between the variables also tend to affect the overall return of the company. The variables to seek out the financial performance of the Automobile companies are return on equity, return on assets and earnings before interest and tax. The independent variables in this case are firm size, inflation, exchange rate, interest rate, GDP growth rate, Money supply, and political

stability.

The relationship between firm size and return on asset is insignificant as the sig value between them is 0.06 which is greater than 0.05. It indicates that firm size does not influence the ROA in case of Automobile industry of Pakistan. Moving towards inflation it has been found that the relationship between ROA and inflation is significant and negative. Correlation value is negative 0.343 which indicates that they are negatively related as higher inflation leads to reduction in return on asset of companies and it also shows that they have a moderate relationship. Moreover, an exchange rate also has significant influence on ROA of Pakistani’s automobile companies. Its correlation value is 0.305 which shows that they have moderate positive relationship. These findings are also supported by Cheungand Sengupta (2013), they found that there is a positive relationship between exchange rate and ROA of Indian’s non-financial firm.

Furthermore, the association between interest rate and return on asset is significant as the sig value between them is 0.005. The value of correlation is 0.268 which shows that they have a positive relation. The association between them seems to be weakly moderate. GDP growth also impacts the return on asset as found from correlation analysis. If there will be increment in GDP growth rate, it will enhance the return on asset as both variables are positively related. Money supply also influences the return on asset and they have negative relationship as when the money supply increases, it reduces the return on asset. Political stability of Pakistan has also taken as an independent variable. Negative 2.5 mean that the country has weak political stability and positive 2.5 indicate the strong political stability. The relationship between political stability and return on asset seems to be significant and positive. The correlation value is 0.253 that explains that they have positive relationship as strong political stability enhances the return of assets of Pakistani Automobile companies.

Return on equity is also a useful indicator to measure the financial performance of the company (Hunjra, Ijaz, and Mustafa, 2014.). It shows that how much return an investors get on their investments. There is no association between firm size and ROE as the sig value between them is 0.17 which is greater than 0.05. If the sig value is greater than 0.05, it means that the relationship between them is insignificant. The correlation value between inflation and return on equity is negative 0.302 which shows that they are negatively related. Higher inflation in Pakistan reduces the return on equity of Automobile companies of Pakistan. The sig value between them is 0.001 which shows that impact of inflation has significantly influence the ROE. The association between exchange rate and return on equity is significant as the sig value between them is 0.000 which is less than 0.05. Correlation value is 0.328 which shows that they have moderate relationship and positively related. Higher exchange rate increases the return on equity of Pakistan’s automobile companies. They study of Elly, and Oriwo, (2013) has also founded that exchange rate is positively influence on ROE of the company.

Interest rate also seems to be positively related with return on equity which means that higher interest rate increases the ROE of Automobile companies of Pakistan. The correlation value shows that they have weak relationship as the value between them is 0.191. The GDP growth has also positively influence the return on equity. It indicates that increment in GDP growth leads to higher return on equity. The relationship between them seems to be moderate as the correlation value is 0.299. Money supply has negatively influence the return on equity of Pakistani Automobile companies. Higher money supply shrinks the return on equity of automobile companies of Pakistan.

Political stability of a country increases the income of the companies. So in case of automobile sector it has been shown that political stability has significantly influences the ROE. The correlation value between them is positive which shows that they are positively related. Higher instability in Pakistan reduces the return on equity of automobile companies of Pakistan.

Earnings before interest and tax is also a key indicator to measure the firm’s performance. It is also known as operating profit which shows that how much a business earns from its core operations (Evanschitzky, Wangenheim, and Wünderlich, 2012.). Firm size has significantly influence the operating profit of the company. Although firm size has not impacted the return on equity and asset but it affects the firm’s operating profit. The relationship between them is positive and moderate as bigger firm size enhances the operating profit of the automobile companies of Pakistan. Inflation affects the operating profit negatively as the correlation value is -0.363. The correlation value shows that the association between them is moderate. Moreover, the sig value is 0.00 that indicates the relationship is significant. Interest rate has also significantly influences the operating profit as the sig value is 0.046 which is less than 0.05. GDP growth rate is positively related to the operating profit to the operating profit of the firms. Higher GDP growth leads to higher operating income of the company.

However, the relationship between money supply and operating income like ROA and ROE. Higher money supply reduces the earnings before income and tax of Automobile companies of Pakistan. Political stability has also effected the company’s operating profit positively. Higher politically stability enhances the performance of the company.

Now the findings of next dependent variable named EPS will be discussed. The relationship between firm size and earnings per share is insignificant. The significance value between is 0.051 which shows that firm size does not influence the earnings per share of the automobile companies of Pakistan. Earnings per share shows the income earn by shareholders on every share. Higher earnings per share is favorable for investors and it attracts potential investors to invest in a particular company. There is a weak relationship between EPS and firm value as the correlation value between them is 0.187. A part from it, it has been found that inflation is negatively related with EPS of a company. Higher inflation of Pakistan decreases the net income of Automobile companies of Pakistan that ultimately results in lower Earnings per share. The sig value between them is 0.000 which shows that earning allocated to every share is affected from an inflation rate. The automobile companies of Pakistan are much concerned with the inflation rate; it impacts the financial performance of the company.

Exchange rate is also the macroeconomic indicator which impacts the performance of Pakistani automobile companies. By seeing the correlation analysis, it shows that there is a significant relationship between earnings per share and exchange rate. The correlation value between them is 0.375 which shows that they have a moderate relationship. The relationship seems to be positive which means that increment in exchange rate leads to increment in EPS. If the country has high exchange rate, then the automobile companies can generate higher EPS. The connection between interest rate and EPS is significant and positive. The sig value between them is 0.00 and the value of correlation is 0.375 which shows that they have a positive relation. The association between them seems to be weak. GDP growth also impacts the EPS as found from correlation analysis. If there will be augmentation in GDP growth rate, it will enhance the EPS as both variables are positively related.

Money supply also influences the earnings per share and they have negative relationship as when the money supply increases, it reduces the EPS of the Pakistani automobile companies. Political stability of Pakistan has also taken as an independent variable and its impact on EPS has been found with the help of statistical tool. The relationship between political stability and EPS seems to be significant and positive. The correlation value is 0.265 that explains that they have moderate and positive relationship as strong political stability enhances the EPS of Pakistani Automobile companies. Overall, political stability improves the economy of the country which ultimately uplifts the financial performance of the companies.

Regression Analysis Impact of Macroeconomic Indicators on return on Equity (ROE)

𝑅𝑂𝐸 = 𝛼 + 𝛽1 𝐼n𝑟 + 𝛽2 𝐸𝑟 + 𝛽3 P + 𝛽4 I +𝛽5 Y + 𝛽6 M +𝛽7 Fs + 𝜖

Where,

ROE = return on equity.

ROA = return on assets.

EPS = earnings per share. EBIT = earnings before interest tax. α = represents the Constant/ Intercept.

𝛽1 𝐼𝑛𝑟= inflation rate.

𝛽2 𝐸𝑟 = exchange rate.

𝛽3 P = political instability.

𝛽4 I = interest rate.

𝛽5 Y = GDP.

𝛽6 M = money supply.

𝛽7 Fs = firm size.

𝜖 = error term

Regression analysis is a statistical tool that helps in understanding the impact of independent variable on dependent variable. It shows which independent variable has significantly influences the dependent variable. From regression analysis, it has been found that impact of dependent variables such as political stability, firm size, interest rate, M2 growth. GDP growth, inflation and exchange rate on ROE is insignificant. The value of R square is 0.119 which shows that 11.9 percent ROE of Pakistani Automobile companies is explained by dependent variable and remaining 88.1 percent is explained by other factors. The coefficient value of inflation is -1.390 which shows that one-unit increment in inflation reduces the ROE by 1.39 units. The sig value is 0.55 which means that the relationship between them is insignificant. The association between exchange rate and ROE is insignificant as the sig value between them is 0.386 which is greater than 0.05. The coefficient value is 0.007 which indicates that if exchange rate increases by 1 unit, the ROE increases by 0.007 units. They both are positively related as increment in one variable increases the other variable.

The association of ROE with all independent variables are insignificant. The coefficient value of interest rate is -.676 which indicates that one-unit increase in inflation rate leads to 0.676 units reduction in ROE as they are negatively related. Moving on to GDP growth, the coefficient value is -3.155 which shows that if GDP growth of Pakistan uplifts by 1 unit then ROE of Automobile companies of Pakistan reduces by 3.155 unit. The relationship between ROE and GDP growth is negative and insignificant. Money supply growth also seems insignificant and negatively related with ROE. From the regression analysis, it has been found that increase the money supply by 1 unit decreases the ROE by 0.576. Political stability is positively related with the ROE as increment of one unit in political stability leads to increment in ROE by 0.73.

Moreover, comparing this finding with the literature, then this finding is not consistent with the finding of the Haider et al. (2018) who found that macroeconomic variables have negative interrelation with the return on equity (ROE), and this shows that characteristics of the Pakistani economy could be different that have influenced the results. However, it is imperative to state that results of primary studies are not significant as compared to the secondary findings; thus the lower sample size, market characteristics and industry characteristics are some of factors that could have led to such results. Therefore, in case of Pakistani context as per the empirical findings of the following study, it can be stated that there is no impact of macroeconomic variables on the return on equity. This means the return on equity in Pakistan is independent from influence of macroeconomic indicators.

Impact of Macroeconomic Indicators on Return on Assets (ROA)

𝑅𝑂𝐴 = 𝛼 + 𝛽1 𝐼n𝑟 + 𝛽2 𝐸𝑟 + 𝛽3 P + 𝛽4 I +𝛽5 Y + 𝛽5 M +𝛽7 Fs + 𝜖

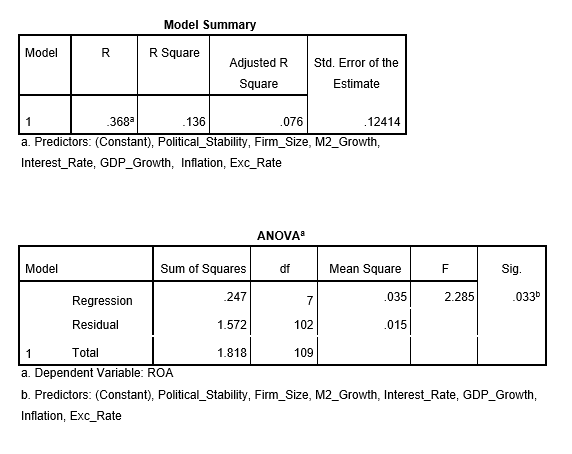

Moving towards the next dependent variable which is ROA. The value of R square is 0.136 which means that 13.6 percent ROE of Pakistani Automobile companies is explained by dependent variable and remaining 86.4 percent is explained by other factors. The impact of firm size on ROA is insignificant. The coefficient value is 7.395E7 which shows that if the firm size increase by 1 unit, ROA increases by 7.395E-7. The coefficient value of inflation is 0.761 which indicates that one-unit increment in inflation reduces the ROA by 0.761 units. The sig value is 0.469 which means that the relationship between them is insignificant.

The association between exchange rate and ROA is insignificant as the sig value between them is 0.702 which is greater than 0.05. The coefficient value is -.001 which indicates that if exchange rate increases by 1 unit, the ROA reduces by 0.001 units. They both are negatively related as increment in one variable reduces the other variable. The coefficient value of interest rate is 0.411 which indicates that one-unit increase in inflation rate leads to 0.411 units’ increment in ROE as they are positively related. Moreover, GDP growth are also positively related to ROA, the coefficient value is 0.051 which shows that if GDP growth of Pakistan uplifts by 1 unit then ROA of

Automobile companies of Pakistan increases by 0.051 unit. The relationship between ROA and GDP growth is positive and insignificant. Money supply growth also seems insignificant and negatively related with ROA. Political instability seems to be negatively related with ROA. The coefficient value is -.019 which indicates that if political stability increases by 1 unit then ROA reduces by 0.19.

Furthermore, comparing the results with the literature then it can be determined that results of the following study are not consistent with the literature since following study provides results as insignificant where all independent variables have insignificant impact on the ROA, implying that impact may be due to random error or by chance. On the other hand, Haider et al (2018) found that there is negative relation of macroeconomic indicators with the ROA, but only inflation has positive relation with the ROA, and this secondary finding is not consistent with findings of following study. This means in case of the Pakistani Automobile industry, ROA is independent from influence of macroeconomic variables.

Impact of Macroeconomic Indicators on Earnings before Interest and Taxes (EBIT)

EBIT = 𝛼 + 𝛽1 𝐼n𝑟 + 𝛽2 𝐸𝑟 + 𝛽3 P + 𝛽4 I +𝛽5 Y + 𝛽6 M +𝛽7 Fs + 𝜖

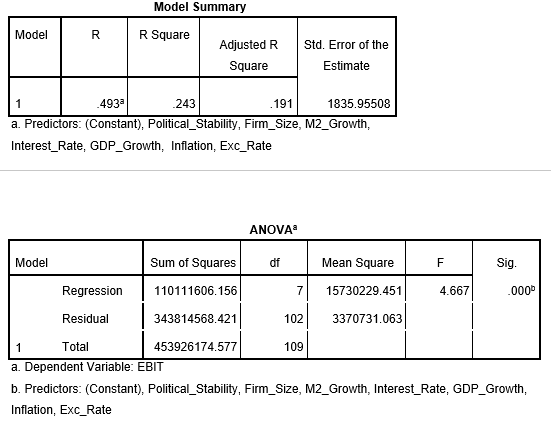

Moving on, next dependent variable is operating profit. The value of R square is 0.243 which means that 24.3% operating profit is explained by dependent variables and remaining 75.7% is explained by other factors. From regression analysis, it has been observed that firm size has significantly influence the operating profit of the automobile companies of Pakistan. Sig value is 0.001 so it is less than 0.05 as it indicates the relationship is significant. The coefficient value between them is 040 which show that the relationship is positive. It indicates that 1-unit increase in firm size leads to 0.4-unit increase in operating profit. The association between inflation and operating profit seems to be negative and insignificant. The coefficient is so high which shows that there would be drastically changes in operating profit due to inflation. The coefficient value is 10977 that indicate one-unit increase in inflation rate leads to 10977-unit reduction in operating profit All dependent variables except firm size such as inflation, exchange rate, interest rate, GDP growth, money supply and political stability have insignificant relationship with operating profit of Pakistani automobiles companies. The sig value between operating profit and exchange rate is 0.662 which shows that the impact of exchange rate on operating profit is insignificant as exchange rate does not influence the earnings before and tax of the companies. Coefficient value between them is 25.168 which mean they are negatively correlated. Exchange rate impacts the EBIT negatively as one unit increases in exchange rate of Pakistan leads to 25.168 reductions in operating profit of Automobile companies of Pakistan.

Therefore, it is evident that this finding is also inconsistent with the study of Haider et al (2018) where author found a negative interrelation of macroeconomic variables with return on equity and return on assets, this implies inflation rate, interest rate and also GDP has negative impact on the return on assets and return on equity. Therefore, it can be stated that a decline in the ROA and ROE is indication of decline net income which means due to macroeconomic conditions EBIT has also decline as result. Hence, it is evident following study’s findings are inconsistent with the secondary findings of the study.

Impact of Macroeconomic Indicators on Earnings per share (EPS)

The regression equation by taking EPS as a dependent variable is

EPS = 𝛼 + 𝛽1 𝐼n𝑟 + 𝛽2 𝐸𝑟 + 𝛽3 P + 𝛽4 I +𝛽5 Y + 𝛽6 M +𝛽7 Fs + 𝜖

ROE = return on equity.

ROA = return on assets.

EPS = earnings per share.

EBIT = earnings before interest tax. α = represents the Constant/ Intercept.

𝛽1 𝐼𝑛𝑟= inflation rate.

𝛽2 𝐸𝑟 = exchange rate.

𝛽3 P = political instability.

𝛽4 I = interest rate.

𝛽5 Y = GDP.

𝛽6 M = money supply.

𝛽7 Fs = firm size.

𝜖 = error term

The R square value is 0.163 which means that 16.3 percent ROE of Pakistani Automobile companies is explained by dependent variables and remaining 83.7 percent is explained by other factors. From regression analysis, it has been found that all dependent variables are insignificant with EPS. The value of coefficient between EPS and firm size is 0.000 which means that 1-unit fluctuations in firm size lead to 0.000 unit in EPS. The relationship seems insignificant as the sig value is 0.436 which is greater than 0.05.

The coefficient value of inflation is -166.29 which shows that one-unit increment in inflation reduces the EPS by 166.29 units. The sig value is 0.436 which means that the relationship between them is insignificant. The connection between exchange rate and

EPS is also insignificant as the sig value between them is 0.535. The coefficient value is

0.491 which indicates that if exchange rate increases by 1 unit, the EPS increases by 0.491 units. It shows that they would be minor change in EPS as earnings are not much sensitive with exchange rate. They both are positively related as increment in one variable increases the other variable.

The coefficient value of interest rate is -45.30 which specifies that one-unit increase in inflation rate leads to 45.30 units reduction in EPS so they are negatively related. Moving on to next variable GDP growth, the coefficient value is -173.29 which shows that if GDP growth of Pakistan uplifts by 1 unit then EPS of Automobile companies of Pakistan declines by 173.29 unit; but effect is unlikely since impact is insignificant. Apart from it, money supply growth also seems insignificant and negatively related with EPS. From the regression analysis, it has been found that increase the money supply by 1 unit decreases the EPS by 65.80 units. Political stability is positively affecting EPS but insignificantly as increment of one unit in political stability leads to reduction in EPS by

5.71 units. The sig value is 0.873 which shows that the relationship is insignificant. Furthermore, it can be analyzed as that this finding is also not consistent with the finding of the Haider et al (2018) implying that EPS is not affected by the macroeconomic indicators significantly. Therefore, Automobile industry of Pakistan in case of selected sample size, it can be stated that macroeconomic indicators have no influence on EPS of the companies.

Discussion of objectives Objective 1: To assess what strategies can firm apply to mitigate the influence of external factors influencing the business

The first objective of the study was the to assess what strategies can firm apply to mitigate the influence of external factors influencing the business, and this objective was completely achieved from the secondary findings of the study where it was conceptualized that the external factors are those that are not in control of the companies, and these factors affect all companies or a specific industry as whole rather than a single company (Adeoye, 2012). Meanwhile, it is also important to state that external factors can affect the operations and decisions of the firm directly or indirectly; and these factors ranges from political instability in the country, legal issues, social problems, and technological disruption and innovation in the industry.

On the other hand, the other macroeconomic factors have also been found to influence the firm’s performance. These both types of factors have significant influence on how firms operate in the country. However, among both types of factors, firm have no control over the macroeconomic factors, and no firm can formulate strategies to mitigate effects of these macroeconomic indicators except through diversification which will be discussed later (Hunjra, et.al 2014). Meanwhile, the political, social, technological, environmental and legal factors can also be managed at some extent to mitigate the effects (Gali 2015). The political instability in the country can restrict the activities of the company, and influence the buying patterns of the consumers in the country. In this condition, concept of nationalism might emerge as result for an international company, but for the national companies the consumer might become more protective to purchase a car or automobile for business due to the instable political conditions.

Therefore, in order to address the political risk in the country, it is critical for the companies to prepare complete plan including consequences of that political instability for the company. This step can help firm to understand extent to which the performance of the company can be affected, hence measures can be taken accordingly (Causevic and Lynch, 2013). Meanwhile, the insurance policy in case of political instability is a most important option that should not be overlooked by the company. It is because, during the political instability including terrorism, war, violence and other factors that could damage the firm’s physical assets can be paid off by the insurance company if all assets of the company are insured with a suitable insurance policy (Asongu and Nwachukwu, 2015; Causevic and Lynch, 2013).

Furthermore, the social problems, and technological problems also emerge due to a fact that increasing awareness among the peoples have become highly concentrated; hence the firms in the automobile industry tend to mitigate the social risks by engaging into the human rights activities, corporate social responsibility (CSR), workplace safety, elimination of corruption, focus on public health, and other social activities. These are activities which can be performed by the firm to mitigate the social risks in the country to avoid influence of this external factor (Adeoye, 2012). Moreover, the technological, environment risk, and legal risk still remains there to affect the firm; and it can be

argued that adoption of latest technology can address the technological factors influence, and insurance policy can mitigate the loss due to the environmental factors.

However, the legal risks can be only be mitigated by following the legal requirements of the company, and that it is also certain that legal environment can also affect firm’s level of profitability in terms of taxation. Hence, it is not possible for the company to mitigate the legal risk except by meeting all legal obligations; where changes into the laws cannot be challenged; but can be requested to government to review the law and its consequences on the industry as whole (CHITECHI, 2014). For this purpose, the association of automobile industry can play an imperative role in arranging the negotiations with the government over the new laws to bring some flexibility.

Furthermore, the other than these issues; the firms face various other types of risks from external factors coined as macroeconomic indicators of the country. However, these indicators are independent from control of any organization or industry since they equally affect the companies either positively or negatively (Gali, 2015; Moro, 2012). Therefore, the mitigation strategies in each factor also tend to vary based on the magnitude, and type of effect. Such as if the inflation in the country increases then price of general goods and services tend to rise in same magnitude; and for manufacturing firms cost of doing business also rises. Hence, to mitigate this risk firms can raise the prices of the vehicles to cover the cost of doing business, and profit margin; but this is not an appropriate or an effective way to deal with the inflation in long-terms.

Therefore, focus on the increase volume of sales can cover the costs of doing business, and provide firm with sufficient profit margin. It is because, increasing sales volume can provide firm with benefit of economies of scale. Meanwhile, third strategy in this regard can be used is increase the production capacity through adoption of technologies, adoption of new techniques, lean management, and total quality management systems in the company. This can reduce the significant costs of the company, and increase production capacity over same number of employees, and company will be able to cover the costs of doing businesses with the competitive parameters in the industry.

Objective 2: To understand that to what extent does the macroeconomic indicator influence the returns of equity (ROE) of the automotive firms in Pakistan

The second objective of the study was that to understand at what extent the macroeconomic indicators influence the return on equity (ROE) of the automotive firms in Pakistan. This objective was also successfully achieved through the empirical tests conducted with help of multiple regressions; where the equation was formed in which return on equity (ROE) was used as dependent variable, and other indicators such as firm size, inflation, exchange rate, interest rate, GDP growth rate, M2 money supply and political stability as independent variables of the study. Firstly, the return on equity (ROE) is an indicator of firm’s performance in terms to return generated by the firm; where the real owner of the firm are shareholders, and all profit after meeting all liabilities and obligations of interest and taxes belongs to the shareholders. Therefore, this measure provides how much return firm generates over the investment of the shareholders.

The primary findings of the study suggest are completely against the secondary findings as Mwangi and Wekesa (2017) found that interest rate, and inflation has effect on the profitability level of the company. Similarly, the political stability also affects the firm directly or indirectly; hence the inflation the interest rate tends to affect the firms’ profitability at some level. However, the primary findings of the study are completely against the secondary findings, where result of the regression reveals that frim size, exchange rate, and political stability has positive effect on the ROE of the automobile companies but effect is not significant at 0.05; and the effect of inflation, interest rate, GDP growth rate and M2 growth rate has negative effect on the ROE but effect is not statistically significant. This implies that no macroeconomic indicator of the Pakistan has significant effect on the ROE of the automobile companies.

It can be determined that rising level of inflation also increases the interest in the country which restricts economic growth given that cost of borrowing increases. However, interest rate is used as technique by government to tackle the higher inflation which could turn into an inevitable damage to economy in longer-term (Omondi and Muturi, 2013). Therefore, the at some extent higher interest rate tend to affect the economy negatively, but the results of the study reveals that interest rate has direct and significant relationship with the GDP growth rate and political stability of the country. Hence, it is also evident that higher interest rate and higher inflation have no significant effect on the return on equity (ROE) in case of automobile sector of Pakistan. This implies that insignificant effect means that shareholder’s return is protected from the external influences that their wealth in either direction, and this finding is also consistent with study of Haider et al. (2018).

Moreover, the return of the investor depends on the how effectively and efficiently firm operates within the industry; where economic indicators do not only affect one specific firm but affects industry as whole (Lim et al, 2015). Hence, the no effect of the economic indicators on the ROE of automobile industry can be attributed to buying behavior of automobile customers in Pakistan; where higher interest rate and higher inflation do not change their buying decision. This implies that sales volume of the company will be same despite unfavorable market conditions for the customers. On the other hand, the findings of the Haider et al (2018) suggests that macroeconomic conditions have negative relation with return on equity, where author specifically found that inflation has positive relation with the ROE, and negative relation with gross profit margin.

Therefore, it is evident that macroeconomic conditions of the Pakistan have no significant effect on the return on equity of the automobile industry. Whereas, the GDP growth rate also found to have negative but insignificant effect on the ROE, which implies that if turns to be significant at 0.05 then it will imply that ROE of shareholders is not affected by even decline in economic growth of Pakistan. However, it is also critical to acknowledge that sample size of the study was very small and time period of the study is also limited to 10 years. This could have influenced the results of the study, where a larger size could also have provided different results.

Objective 3: To find out the extent to which the macroeconomic factors affect the returns on assets (ROA) of the automotive firms in Pakistan

The third objective of the study was to find out extent to which the macroeconomic factors affect the return on assets (ROA) of the automotive firms in Pakistan, and this objective was also successfully achieved through correlation and regression analysis. Return on assets (ROA) is an effective measure of firm’s net profit comparative to total assets of the company. Therefore, an increase into the net profit and increase into the total value of the assets can influence the ratio in either direction. Meanwhile, the correlation analysis reveals that relation of ROA with firm size is positive and insignificant, negative significant with inflation, positive significant with exchange rate, positive significant with interest rate, positive significant with GDP growth rate, negative significant with M2, and lastly positive significant with political stability. Based on the results of correlation, it can be determined that exchange rate, GDP growth rate and political stability positively influence the return on assets (ROA); whereas the inflation and M2 negatively influence the ROA of the automobile companies in Pakistan.

It is sufficient evidence to claim that the return on assets (ROA) of the automobile companies of Pakistan is influenced by macroeconomic indicators in both directions but subject to magnitude and nature of effect. Moreover, the regression results reveal that firm size, interest rate and GDP growth has positive but insignificant effect on the ROA; whereas the inflation, exchange rate, M2 growth rate, and political stability negatively influence the ROA of the automobile industry of the Pakistan. However, as per secondary study conducted by NDEGWA (2017) and Haider et al (2018) that macroeconomic conditions negatively influence the ROA and inflation rate positively affects firm performance, but higher interest rate negatively. Therefore, it can be stated that a positive influence and negative influence of interest rate on performance of the firm can be described as that higher inflation increases prices of general products, and firm also have increased profit, where higher interest rates in the country is due to existence of inflation in long-term, and long-term inflation tend to have negative effect on the firm performance because firms cannot recover cost of doing business.

Furthermore, it is found return on assets (ROA) has not been significantly affected by the macroeconomic conditions of the country; which implies that performance of the automobile industry is independent from influence of external factors. However, findings of PEHLİVANOĞLU and RİYANTİ (2018) are different who found that real GDP has positive influence on car sales, but GDP per capita, inflation and exchange rate negatively influence the sales of car in US, China, Japan and Germany. In contrast, Tha et al (2013) found that there is no significant long-term effect of macroeconomic indicators of the Malaysia with sales of Passenger Vehicles. This implies that sales of passenger vehicle are not affected by the macroeconomic conditions given that it is necessity and has to be fulfilled at any cost irrespective macroeconomic conditions. Similarly, findings of present study also are consistent with this study that financial performance of the automobile sector of the Pakistan is not significantly affected by the macroeconomic conditions of the country.

Chapter Summary

This chapter has contained into the four parts, in firsts section descriptive statistics has been implemented which include the graphical representation to analyses the characteristics of the data, and observe the patterns. The mean EPS of the selected automobile companies of Pakistan is 17.89 with standard deviation of 24.64 which is higher and implies that there is a significantly difference between the EPS of the given companies. The minimum and maximum EPS has been found as 15.62 and 121.64 within the companies. Moreover, the mean ROA is 9.36% % with standard deviation of 12.91 while mean ROE is 15.45% with standard deviation of 28.33%. The mean EBIT has been observed as 1466.06 million with standard deviation of 2040.70 which is also higher than mean value, and minimum EBIT was -1416.20 million and maximum EBIT was 870 5 million.

In second section, the correlation and regression analysis have been conducted to address the primary research questions. The independent variables for this analysis were firm size, inflation, exchange rate, interest rate, GDP growth rate, Money supply, and political stability whereas the dependent variables are ROA, ROE, EPS and EBIT. The relationship between firm size and ROA is insignificant as the sig value between them is 0.06 and that the relationship between ROA and inflation is significant and negative.

Moreover, an exchange rate also has significant impacted on return on asset of Pakistani’s automobile companies as they have moderate positive relationship. Moving on, the association between interest rate and return on asset is significant as the sig value between them is 0.005 and they have positive relation. Money supply also influences the ROA and they have negative relationship as when the money supply increases, it reduces the ROA. Furthermore, the association between political stability and ROA seems to be significant and positive as it shows strong political stability of Pakistan improves the ROA of Pakistani Automobile companies. Moving on to next variable ROE, it has been observed that firm size, exchange rate, interest rate, GDP growth, and political stability are positively related with ROE whereas money supply and inflation are negatively correlated with ROE as per correlation analysis. Same case with

EBIT, as all variables except money supply and inflation are positively correlated with

EBIT. Likewise, money supply and inflations have only negatively correlated with EPS. Regression analysis has been found that R square value is 0.112 in case of ROE whereas value of R square in case ROA, EBIT and EPS was 0.125, 0.217 and 0.148 respectively. The R square value shows the percent of dependent variable is explained by independent variables. All independent variables have insignificant relationship with ROE. Likewise, all macroeconomic variables have not influenced the ROA of the automotive firms of Pakistan. In case of EBIT, only firm size significantly impacts the EBIT of the companies. Moreover, it has also been found that all given variables has insignificant relationship with EPS.

In last part, detailed discussion has been based on the primary findings of the study, and explained the objective of the study. The first objective of the study was to assess what strategies can firm apply to mitigate the influence of external factors influencing the business and it has been successfully achieved from secondary researches. The second objective was to seek out understand at what extent the macroeconomic indicators effect the return on equity (ROE) of the automobile of Pakistan. This objective has been attained through the empirical tests conducted with help of multiple regressions. The third objective was to understand the effect of macroeconomic factors on the return on assets (ROA) of the automotive firms in Pakistan. It has been successfully achieved through regression and correlation analysis.

View More Samples

WhatsApp Now

Get Instant 50% Discount on Live Chat!

WhatsApp Now

Get Instant 50% Discount on Live Chat!