- Dissertation Topics (185)

- Accounting Dissertation Topics (8)

- Banking & Finance Dissertation Topics (10)

- Business Management Dissertation Topics (35)

- Economic Dissertation Topics (1)

- Education Dissertation Topics (12)

- Engineering Dissertation Topics (9)

- English Literature Dissertation Topics (3)

- HRM Dissertation Topics (3)

- Law Dissertation Topics (13)

- Marketing Dissertation Topics (9)

- Medical Dissertation Topics (7)

- Nursing Dissertation Topics (10)

- Other Topics (10)

- Supply Chain Dissertation Topics (2)

- Research Topics (16)

- Biomedical Science (1)

- Business Management Research Topics (1)

- Computer Science Research Topics (1)

- Criminology Research Topics (1)

- Economics Research Topics (1)

- Google Scholar Research Topics (1)

- HR Research Topics (1)

- Law Research Topics (1)

- Management Research Topics (1)

- Marketing Research Topics (1)

- MBA Research Topics (1)

- Medical Research Topics (1)

- Guide (63)

- How To (32)

- List (20)

Table of Contents

CHAPTER 4: RESULTS

Introduction

The purpose of this chapter is to represent the valuable results that have been obtained through the use of questionnaire and to carefully analyse them as a result to obtain a broader perspective of the research topic. In order to obtain relevant data for the research qualitative interviews had

been conducted from respondents that are supposedly working in the FAB. At first a demographic analysis has been conducted in order to comprehend the nature of the respondents and following it is the evaluation of the responses provided by them which are related to the topic.

Demographic Analysis

Gender and Age Demography

In this study a total of 23 respondents had been selected in order to come up with suitable answers to the questions that have been mentioned in the research. Out of the total 23, only were male and the remaining 8 were females. This a clear representation that bank is trying to balance the number of males and females in the organisation to show equality in the workforce.

From the total number of 23 respondents there were 7 individuals that were 25 to 34 years, 5 individuals from 35 to 44 years old, another 5 respondents belonged from the 45 to 54 years age group, 5 belonged from the 55 to 64 years group and 1 respondent belonged from the age 65 or older group. This represent the diversity of age group in the bank and the individuals that were being interviewed had adequate knowledge of the questions that were being asked from them related to the case study of the FAB.

Experience

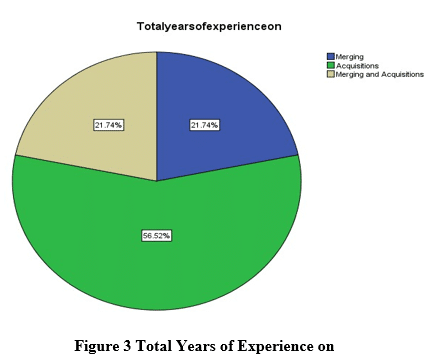

It was necessary to determine the experience of the respondents in order to understand the expertise and knowledge they possessed regarding the case of FAB. A total of 27 candidates had been selected for the interviews out of which 5 had information regarding merging, 13 had knowledge of acquisitions and 5 had knowledge of merging and acquisitions. This represents that the respondents had been familiar of both the terms mergers and acquisitions and were able to answer the questions without any hindrance. Out of 23, only 13 respondents had experience of 12 years, 6 individuals had an experience which lied between 2 to 5 years at hand, 2 had an experience of 6 to 8 years while only 1 respondent had an experience of more than 10 years. The experience of the individuals was dependant on their position and age. Furthermore the researcher also inquired of the total years of experience on the current position of the organisation. Out of the total 23 respondents 5 individuals had been on the same position for 1 year and were looking forward for a promotion. 9 out of 23 had answered that it had been 5 months of experience on their current position, 6 had answered that it had been 9 months of experience on their current position and 3 had answered that they have had experience of 1.5 years on the same position. When questioned regarding the total years of experience while working with banks or in the financial sectors, 10 individuals had answered that they had experience of 1 to 3 years, 4 respondent that they had experience of 4 to 5 years, 7 respondent that they had experience of 6 to 7 years and lastly 2 respondent that they had experience of 8 to 10 years in the banking sector. This represents that the individuals that had been chosen for the research had adequate knowledge of the banking sector and their current position which made it easy for them to answer the questions of the questionnaire.

Education level

The researcher was also keen on investigating the education level of the respondents that were capable of answering the questions of the research. Out of the 23 respondents only 1 had a study of high school, 3 had received a diploma, 10 had done their bachelors, 8 had achieved a master’s degree and 1 was a PhD. Their knowledge regarding the case of FAB had been beneficial enough to answer the relevant questions that had been mentioned in the research in order to formulate recommendations based upon the research problem. It had also allowed to give a detailed expression of the research aims and objectives.

General Examination

Merger and acquisition require sound knowledge and strategic planning on the part of companies that are involved in the process. However, certain factors along with stakeholders play a very significant role in ensuring that the process of merging and acquisition is undertaken and implemented successfully. Firms are also identifying measures and frameworks for ensuring that their strategic objectives related with merger and acquisition are achieved. Nonetheless, primarily it is important to find how different stakeholders associated with merger and acquisition considers about the overall process and what are their roles in it as well. Therefore, the researcher has asked a number of general questions from the respondents in order to examine their concerns regarding merging and acquisition as well as their role in the process. For this purpose, both open-ended and close-ended questions have been asked. The researcher has also asked about the main drivers of merger and acquisitions. The results related to the general questions are analysed below:

View of respondents

First, the researcher asked the respondents regarding their views on merging, acquisition and merging and acquisition. In response to answering this question, the respondents have also highlighted the differences between merging, acquisition and M&A. One respondent has elaborated,

“Well, in my opinion, mergers is the process associated with the mutual consensus amongst business entities where they decide to collectively manage as well as run two or more companies through combining together and operating as one single entity.”

Another respondent has highlighted,

“Merger is obtained through the sharing and investment of shared as well as other funds. It can also be regarded as the merger of set of companies, it can be one or more than one, and thereafter the parties involved commit to maintenance of the new company’s image as well as their value”

The respondents have highlighted regarding merger as the way of combining the two firms together in the form of their investments, funds, shares etc. with their mutual consensus to operate as a single organisation. The respondents of the study have also provided the difference between merger and acquisition. One of the participants has stated,

“A merger is initiated when two separate businesses are prone to combine their forces in order to generate a new and single combined organisation. On the other hand, acquisition is considered as the takeover of one business by another. Hence, M&A is regarded as the way of reaching to an optimal level of market share and to also create shareholder value”

The respondents have differentiated amid merger and acquisition and considered merger as the way of amalgamation of two business organizations whereas acquisition is the process of takeover of a business completely where the merged the business company ceases to exist. Hence, M&A is regarded as a combined effort where the management of both organisations takes several initiatives in order to generate significant market share, market value and shareholder value.

Strategy For Merging

The researcher has asked the respondents if they have a strategy for merging in their organisation. This question was represented as a close ended question where respondent was requested to answer yes or no. For a successful merger, it is highly important for the management to have a certain strategy in order to ensure that risks of failure are effectively mitigated. The results are provided in the following table indicating that 16 respondents said yes while 7 respondents have stated no as their answer.

Strategy For Acquisitions

The respondents were also asked if they have a strategy for acquisitions. This question was represented as a close ended question where respondent was requested to answer yes or no. Strategic acquisition is a highly important mean for development and growth of the business and it also leads towards the acquisition of market and sales as well as easier and convenient financing for future undertakings along with immediate savings. The table provided below is indicating the results of the respondents indicating that 21 respondents said yes while 2 respondents have stated no as their answer.

Strategy For Merging And Acquisitions

The researcher has asked the respondents if they have a strategy for merging and acquisition in their organisation. This question was represented as a close ended question where respondent was requested to answer yes or no. A strategic merger and acquisition requires a specific aim to create synergies for a long run that can lead to increased customer base, augmented market share and increased corporate strength of the organisation. The results are provided below indicating that 19 respondents said yes while 4 respondents have stated no as their answer.

Role On Merging

The respondents have been asked regarding their role in merging. Employees and managers play a very important role in the implementation of the strategy related with merging. This was highlighted by one of the respondents,

“I am usually responsible for forecasting the effects of merger on the organisation including its assets, market share and shareholder value”

The management of the organisation is also responsible for establishing synergies that can lead towards facilitating financial and corporate control as well as measuring the ability of the firm to play its part in merger. This was also further elaborated by one respondent,

“I have focused on identifying the efficiencies of the firm in terms of how it will be able to establish control on its financial and corporate level after merger”

The managers and CEO of the organisation play a very important role in communicating the objectives of merger. This was highlighted by one respondent, who said,

“I ensure that the objectives of merger are effectively communicated to all levels of the firm. It is important to focus on strategic dimension which I make sure undertake through the lens of corporate governance.”

Another respondent highlighted their role,

“Well, I observe the screening of potential target companies that can be used for merger and I do it prior to the announcement of merger as well as before its implementation.”

It indicates that each stakeholder working in the firm requires taking thorough assessment of why the merger is taking place and which company should be chosen for merger. Furthermore, the responses have also indicated that communication of the objectives of merger prior to its implementation is also significantly done by the respondents as a part of their role during merger.

Role on acquisitions

The respondents were asked about their role in acquisition. For this, one respondent highlighted,

“I ensure to maintain adequate authority whenever my organisation undertakes the process of acquisition. It is because I need to make sure that there is no issue pertaining in the process and problems are effectively resolved”

Another respondent has elaborated,

“Well, it is essential to guarantee that during and after acquisition, the functions of the acquiring firm are handled and individuals are provided with clear focus to play their part in the certain business functions”

For acquisitions, managers play their significant part in ensuring that the staffs are committed to the overall mission and vision related to acquisition. The responses have also indicated that stakeholders to the acquisition play their essential role in mitigating the risk of failure as well as risks associated with the problems generated by individuals working in the acquired and acquiring organisations. One of the respondents has also highlighted,

“I am usually responsible for establishing measures in after-acquisition period. This period is very important for us because in this period we analyse if the acquired firm is fully ready for the adoption of new culture and new ways of working”

While explaining their role in the after-acquisition period, another respondent elaborated,

“Well, after-acquisition phase is the most difficult one and I am the one responsible for keeping discipline in this phase. Such as, I make sure that the functions of the firm are not compromised, promising results are achieved and if necessary I also undertake meetings as well in order to interact with new employees.”

The results have indicated that their role in acquisition is significant but differ from person to person. For instance, some are responsible for communicating concerns where some are responsible for dealing with the issues in after-acquisition period.

Role On Merging And Acquisitions

The respondents have also asked about their overall role in M&A. One respondent has highlighted,

“Well, as I have mentioned earlier, I take care of all the financial elements during M&A. I prepare a financial report that indicates the current performance of the organisation and also shows the forecasting of the performance after merger.

Another respondent highlighted,

“Well, from the point of announcement to the point of closing date, I make sure that the firms are aware of the legal requirements and are also adhering to all the requirements required by law during and after M&A”

One of the respondents also stated,

“I always make sure that the team is on one page before, during and after undertaking M&A. I also ensure that all the negotiations amongst the merging companies are undertaken properly. For instance, investors, consultant management, specialists and employees are given specific task in the process of M&A for ensuring that implementation is done smoothly.”

The above responses show that during M&A, managers and employees are responsible to undertake different tasks. For instance, one of the important tasks is the forecasting of financial performance of the firm after M&A. Specific employees also play a significant role in ensuring that the firm is able to comply with all the legal requirements associated with M&A.

Main Drivers For Merging And Acquisitions

The respondents have also asked regarding the main drivers of merging and acquisition. It is important to comprehend why organisations undertake M&A and what are the motivations behind incorporating such measures. While elaborating this, one respondent highlighted,

“I think that the foremost driver for M&A is the synergy of company’s operations and it happens when the factors such as skills and resources of two organisations are combined”.

Another respondent has highlighted,

“Well, the major driver for M&A is the strategic goal where the firm is inclined towards achieving significant growth and another reason or driver is diversification for which companies undertake M&A.”

The major driver for M&A is to optimise the operations of the company through which significant growth can be achieved. Firms are prone to M&A if they want to combine their resources and skills if they want to minimise cost and increase the strategic value of the firm. This has further been elaborated by one of the respondents,

“High cost is the major issue that economies of scale face and due to this issue firms undertake M&A because when companies merge their costs are also divided and shared to a significant level”

The response has indicated that with the minimisation of costs, the firms enable themselves to take significant strategic decisions that can further lead to higher value of the firm. Overall responses indicate that firms are able to incorporate M&A when they are prone to increase their growth and augment their operations.

Characteristic and Adoptions – Merging and Acquisition

The following section was designed to address the benefits of merging and acquisition and the risks which are related to it. It is important as it covers the importance of change management approaches which can be observed in the merging and acquisition. Furthermore, it also provided an insight about the considerations which can be taken to avoid these risks. Factors which are related to the failure of merger and acquisition in the banking sector of UAE were analysed and the people who are involved in the process were also identified. Finally, recommendation were also provided by some employees for effective merging and acquisition procedures which can improve its implementation.

Main Benefits Of Merging, Acquisitions And Merging And Acquisitions

When the respondents were asked about the main benefits of merging, acquisitions and merging and acquisition, the responses contains a mix of cultural development, improved communication and demographics of the employees. One employee responded that

“With mergers, one key benefit which can be identified is the diversification of the cultures. If one of the firms pay significant attention towards the involvement of varied cultures, the employees of the other companies can be benefitted from it.”

Another respondent highlighted the enhancement of communication by quoting,

“The communication process in the mergers and acquisition improves because the different methods of communication are adopted. It is because the employees belong to different backgrounds and a single method cannot be adopted by everyone”.

One more employee responded that,

“Demographics are also a core benefit which is resulted from the mergers and acquisition. The employees related to different background and experiences can collectively contribute to the success of the organisation.”

The responses generated from the employees can conclude that the mergers and acquisition are indeed an effective way to enhance the cultural adaptation in the organisation which also leads to the expansion of the business.

Risks of Lacking Benefits For Merging, Acquisitions And Merging And Acquisitions

In response to the risks which are related to the benefits of merging and acquisition, following responses were gathered from the employees.

The CEO highlighted that, “Many have seen cultural conflicts and are the most recognized explanation of the disappointment of mergers and acquisitions. Employees are the central quality of an association and if there is no incorporation between them, the association is intended for self-destruction. Consequently, the similarity of the two organisations must be verified before the merger.”

One employee quoted that, “An ideal concept must be achieved before consolidating or obtaining many confusing estimates, which is important for both organisation. Control over the calculation or errors in the estimate can lead to overwhelming setbacks of the consolidated item.”

Another employee responded that, “The association may lose several representatives during a merger. Impotence to assess the estimate of their representatives leads organisations to end up with inappropriate people.”

The responses suggested that the companies should take care about the legal risks and motivation level of employees when entering into mergers and acquisition process.

Considerations / Strategic Actions Taken To Avoid The Risk

The participants of the study were also inquired about the actions which they think should be taken by the companies to counter the above mentioned risks. One employee responded that,

“It is significant that organisation does not take short cuts during the process. Contractual experts who know the company, they can organize better arrangements for it because they are sincerely connected and can press with more enthusiasm for dealers’ concessions.”

Furthermore, a response generated by one more employee quoted that,

“Disappointments of mergers and acquisitions are often the result because buyers focus heavily on cooperative energy costs and lose focus around preservation or profit potential. Customer maintenance at management offices is at great risk after a merger or security. Clients will be deceived, so it is important that the contracting company move quickly to ensure that administrative levels increase or exceed what they have become accustomed to.”

Barriers And Challenges To Do Merging And Acquisitions

As for the barriers and challenges which are faced by the companies during mergers and acquisitions, respondents highlighted lack of communication, employee retention and cultural challenges as some of the major factors. A respondent highlighted that,

“Talking with employees, involving them and creating a culture in which they can thrive are essential elements of reconciliation. When mergers and acquisitions are made, the representatives and the board are generally unclear. Fear and lack of responses prevent senior management from providing the data employees need to divert their activities to the mixed organisation.”

Another participant quoted that,

“Employee retention can be a problem as a greatest number of trusts can be a danger. Of course, numerous mergers and acquisitions have similarities with retention issues, which are the result of negative moods that representatives feel. This may include vulnerability to the fate of the association’s course, professional stability, understanding of the lack of credibility of the administration and feelings of disorder due to the lack of correspondence.”

Critical Success Factors For Merging And Acquisitions

Following are some of the critical success factors which were highlighted by the respondents for merging and acquisition.

- The common trust between the administrations of the two organisation ensures that exchanges develop smoothly, which increases the chances that the agreement will be successful.

- Despite the variables mentioned, the nature of the assessment after total resistance is significant. The constant persistence of mergers and acquisitions is a thorough investigation of the historical, strategic, cultural and money-related reports of an association and is important to obtain a satisfactory valuation. A bad valuation can lead to an increase in value, so that the merger or the guarantee seems a disappointment, looking back, anyway it simply continues.

- Experience with previous mergers and acquisitions can be a huge job, as indicated by certain business analysts, while others struggle because it has no impact. Most importantly, the supervisory team benefits from previous organisation: the experience alone does not offer opportunities for progress. A previously bombed tender, for example, can make executives cautious in supplying a different band along with data in a clear order of transactions. If the other party is denied the opportunity to form an unequivocal perspective on the acquisition, this can confuse them.

Failure Factors Of Merging And Acquisitions

The respondents were asked about the factors which resulted in the failure of the merging and acquisition. For this, they quoted limited involvement from the owners, difference between theoretical and practical valuation, lack of clarity, cultural integration issues and negotiation errors. One respondent highlighted that,

“An important test for any merger and acquisition is to join the merger. A cautious evaluation can help with recognized key representatives, companies and key articles, difficult procedures and problems affecting bottlenecks, etc. With the help of these key base regions, productive procedures must be planned for clear reconciliation, with the support of advice, automation or at least the appropriation of alternatives that are fully explored.”

One participant highlighted that,

“Cultural integration is very clear in the global mergers and acquisitions negotiations, and a legitimate system must be devised to opt for coercive coordination that neglects social contrasts or allows provincial / neighbourhood organisations to direct their individual units, with clear objectives and methodology to take advantage of.”

People involved in merging and acquisitions decision-making

According to the responses gathered from the participants of the study regarding the key player involved in the mergers and acquisition, following members were highlighted along with their roles.

- Business buyer: Typically CEO of acquiring company (depending on size of acquirer and acquired). Makes strategic decision to pursue acquisition strategy in general, and then particular company in specific

- Corporate development: Executes and orchestrates the mechanics of the acquisition process from buyer side

- Buyer Banker: Optional, in the event buyer is not large enough to have full time corporate department

- Corporate legal internal: Arranges the legal negotiations in the acquisition with seller counsel and (optional) external buyer counsel

- Buyer external legal: Executes mechanics of legal review on behalf of buyer legal

- CFO/Business analysis: Performs business and financial analysis of acquisition impact/scenarios/revenue/growth projections for buyer post acquisition

- Board of Directors: Oversight for acquisition strategy in general, only involved at highest levels to approve acquisition, especially if purchase is for stock or substantial cash/debt. May be more involved in smaller buyers.

Recommended decision criteria for merging and acquisitions adopting

| Criteria | Description |

|---|---|

| Direct Negotiation | The procedures for mergers and acquisitions were described by direct agreements between meetings, without the intermediate person of external specialists. The use of monetary and legitimate guides in the scheme by the organisation obtained did not constitute a deterrent until the end of the exchange. Despite what can be expected, the use of specialists to help with specialized problems identified with the activity, identified important things of exchange and contributed to its effective completion. |

| Performing Original Functions | The climate of certainty, combined with the search for a more prominent integration among organisations that satisfy in vital complementarity, has allowed the pioneers of acquired organisations to continue using their unique capabilities in the execution of mergers and acquisitions changes, such as senior executives of organisations had changed their jobs and began to respond at a more important level. |

| Strategic Alignment | Finally, another point raised by the respondents was the strategic alignment due to the business combination. Organisations resulting from mergers and acquisitions grew in better aggressive conditions. The support with an exchange of commercial mix allowed to gain a significant advantage due to the combination of innovation, information, individual, related to the money and the procedures that arise from their parent organisations. In the meetings it has allowed them to perform an authorized reconfiguration, which has made the management of these organisations higher than ever. |

The above table shows that the respondents considered the direct negotiation, performing original functions and strategic alignments as the main parts of the decision criteria involving mergers and acquisitions. It is because these factors cover all the necessary procedures which are important for the successful completion of mergers.

Role of M&A in enhancing banking and financial sector efficiency

| Role | Description |

|---|---|

| Cost Benefits | Essentially as a result of economies of scale, improved operating costs, simplification risks and less expensive access to money-related subsidies. |

| Economies of Scale | Comparatively, economies of scale are gradually being activated to meet the apparent potential of a significant reduction in notable redundant labour costs, mainly by eliminating coverage departments and incorporating administrative, authorized and promotional capabilities. The emergence of data innovation (IT), internet and telephone banking is an essential engine for the union in all aspects to ensure that such innovation favours larger companies in light of the huge initial general costs compared to the activity size of smaller companies. |

| Firm Efficiency Improvement | Mergers have been sought as a way to reduce wasteful aspects in associations. The essential driver of these inefficient aspects has all the features of specialized waste, for example, through the use of abundant inputs. This offers impressive potential to achieve cost savings through mergers, since securing banks is more effective in ethics than in objectives, offers better and increasingly productive administrative trials, procedures and predisposition for less qualified banks. In any case, this procedure is not without complexity if it was not basically taken care of and admirably affected productivity, without improvements or disintegration after joining. |

| Cheaper Access to Financial Sources | Larger banks do so largely because they are considered, sometimes without a doubt, safer due to the seemingly more serious expansion of danger in one place and the inalienable belief that huge banks are too big to be short. As a general rule, markets accept that in an emergency, large banks will receive more expert help than smaller banks. In other words, administrative specialists are reluctant to give a large bank the opportunity to fail due to the high social costs associated with that disappointment. |

Cost Benefits, Economies of Scale, Firm Efficiency Improvement and Cheaper Access to Financial Sources are some of the major roles identified by the respondent which enhanced the banking sector. It was also identified that the application of M&A is significantly beneficial for the banking sector due to the sharing of risk and opportunities.

Importance of Change Management in M&A

| Importance and effect | Low | Medium | High | Justifications / note |

|---|---|---|---|---|

| Level of Effect | 8 | 4 | 11 | Some members of the traditional M&A deal team simply will not appreciate the importance of change management and that's why it's incumbent upon the CEO and other top executives to exercise leadership. Quite simply: if M&A deals were purely quantitative and legal exercises, then the failure rate of these transactions would not be so high. Financial models are based on assumptions and are only as useful as the data on which they are based. |

| Level of Importance | 5 | 8 | 10 | How will leaders of the newly integrated organisation lead change? What governance model will be put in place? How will progress be measured? It is one thing to identify the change management risks associated with a deal; it’s another thing entirely to have a strategy and plan to manage those risks. Considering how the newly integrated company will overcome these challenges throughout the organisation is imperative |

From the above mentioned table, it can be identified that the level of effect which is created by change management process on M&A is responded by 8 for low, 4 for medium and 11 for high. This shows that a considerable effect can be identified on M&A process as the change management often involves the inclusion of major departments of a company. For level of importance, 5 responded for low, 8 for medium and 10 for high. It means that the change management is important for the business so it can keep up with the global world.

Importance of Change Approaches during M&A Decision making

| Changes Approach | Low | Medium | High | Justifications / note |

|---|---|---|---|---|

| Integration Plan | 5 | 8 | 10 | The first step should be the creation of a working group, including the top managers of both associations. Instead of focusing on daily exercises, they should be responsible for easily transferring M&A exercises. It is advisable to inform employees immediately. |

| Clear Vision | 3 | 10 | 10 | The senior official of the association must establish objectives, qualities, vision and strategies of the new organisation. You must communicate clearly to the association. |

| Understanding Cultural differences | 5 | 9 | 9 | Culture has an important influence to achieve and disappoint a new structure, in particular due to more extensive mergers and acquisitions. Pioneers should have the ability to induce people to abandon their usual familiarity and acclimatized standards and recognize new ones. In addition, to achieve this, the pioneer must be in a consistent part of the representatives. Invest energy with them, discover them, what bothers them, what gives them energy, helps pioneers to make individuals recognize the new culture. |

| Employees Involvement | 3 | 5 | 15 | This offers both sides of the employee the opportunity to gather their vision of the association of others. At the time they work together, they share information about their individual procedures, frameworks, spending plan, staff and activities. Building trust is essential to develop learning. Until the different parties trust each other, they will not discover sensitivities. |

| Customer Focus | 6 | 6 | 11 | In today's world, it is important that organisations share the future guide with the current client and guarantee the client that they will continue to provide assistance, personnel support and will continue to complete the sales staff as they did before. This will make the customer sure about their purchase request. |

The above table shows that that for the integration plan, 5 responded low, 8 responses were medium and 10 responses were high. In the case of clear vision, the responses for low dropped to 3 and medium goes up to 10. High is also showing 10 as the clarity of vision do effect the change approach dramatically. Understanding the cultural differences have a number of 5 for low and 9 for both medium and high. The employee’s involvement highlighted 3 respondents answered low, 5 answered medium and 15 responded for high. It means that the change process will be effective if the employees are fully involved in it. Finally, the customer focus showed 6 for low and medium and 11 for high highlighting the importance of customer needs in the change process.

External Factors level of importance to decide on merging and acquisitions

| SR# | External factors | Medium | Justifications / note | ||

|---|---|---|---|---|---|

| Low | Medium | High | |||

| 1 | Globalisation | 8 | 5 | 10 | M&As have gained importance due to globalisation, rivalry and coordination of the national and global business sector, forcing organisations to direct M&As to obtain more benefits and greater wealth for investors for several reasons. The amount of M&A has undergone solid development in many emerging economies as a result of the process of monetary progression. |

| 2 | Market Opportunities | 10 | 2 | 11 | The organisation distinguishes products and services for companies. The business that one acquire must have the ability to give him products or services that he can sell through his own distribution channels. The advantage of this is the ability to generate more revenue in business. With broad market opportunities, the company can further expand its compass and increase its participation in the total industry |

| 3 | Reducing Competition | 5 | 8 | 10 | The moment the industry share and the region is built, it becomes more serious for competitors to compete. They must be satisfied with a small part of the total industry, stop the operations or become a new subsidiary for a larger organisation. At the moment when mergers can run at lower costs than their rivals, they can reduce their costs, causing others to fail because they cannot compete in an estimated war. |

The above presented table showed that the respondents quoted 8 for low, 5 for medium and 10 for high in case of globalisation. It is because the globalisation has a major impact on the mergers and acquisition. Furthermore, market opportunities have 10 for low, 2 for medium and 11 for high showing that the M&A has better market opportunities as compared to the others.

Finally, reducing competition is showing 5 for low, 8 for medium and 10 for high.

Internal Factors level of importance to decide on merging and acquisitions

| SR# | External factors | Level Of Importance | Justifications / note | ||

|---|---|---|---|---|---|

| Low | Medium | High | |||

| 1 | Resources | 5 | 8 | 10 | This powerful motivation is the primary reason why M&A activity occurs in distinct cycles. The urge to snap up a company with an attractive portfolio of assets before a rival does so generally results in a feeding frenzy in hot markets. Some examples of frenetic M&A activity in specific sectors include dot-coms and telecoms in the late 1990s, commodity and energy producers in 2006-07, and biotechnology companies in 2012-14. |

| 2 | Process | 7 | 8 | 8 | Companies also merge to take advantage of synergies and economies of scale. Synergies in the process occur when two companies with similar businesses combine, as they can then consolidate (or eliminate) duplicate resources like branch and regional offices, manufacturing facilities, research projects, etc. Every million dollars or fraction thereof thus saved goes straight to the bottom line, boosting earnings per share and making the M&A transaction an “accretive” one. |

| 3 | Capabilities | 6 | 7 | 10 | Companies also engage in M&A to dominate their sector. However, a combination of two companies would result in a potential monopoly, and such a transaction would have to run the gauntlet of intense scrutiny from anticompetition watchdogs and regulatory authorities. |

The above table has represented resources, capabilities and processes as the major internal factors for mergers and acquisition. The resources has 5 for low, 8 for medium and 10 for high showing that the companies involving in mergers have sufficient resources. For process, 7 is for low, 8 is for medium and 8 for high representing that the operational activities should be aligned with the M&A. Finally, capabilities are showing 6 for low, 7 for medium and 10 for high representing that the firms must be aware with the M&A procedures.

Implementations - Merging and Acquisitions

This section covers the implementation framework for M&A and it covers the practices that should be undertaken in pre-implementation, during implementation and post-implementation phase of M&A. It is important to examine what the respondents consider regarding the practices that should be incorporated throughout M&A processes.

Good practice of Pre Implementation stage merging and acquisitions with the level of importance

The respondents were asked about choosing the level of importance for the good practices of pre-implementation stage of M&A given in the questionnaire. The respondents were asked to choose from the options such as low, medium and high. The responses are given below:

| SR# | External factors | Level Of Importance | Justifications / note | ||

|---|---|---|---|---|---|

| Low | Medium | High | |||

| 1 | Strategic Planning | 2 | 5 | 16 | Strategic planning is considered to have high importance in the preimplementation phase because of the initial stage in which plan and a specific strategic framework is significantly required |

| 2 | Communication of Objectives | 8 | 10 | 5 | Communication of objectives is considered to have medium level of importance in the pre-implementation phase because the stakeholders including employees of the firms are required to understand the reasons behind M&A and play their part accordingly. |

| 3 | Preserving current value of assets | 2 | 5 | 16 | Preserving current value of assets is considered to have high level of importance in the pre-implementation phase because it is important to ensure that the firm is able to preserve its financial performance after the process of M&A |

| 4 | Legal know-how | 3 | 8 | 12 | Legal know-how is considered to have high level of importance in the preimplementation phase in order to make sure that negotiations for M&A are undertaken as per the given legal requirements. It will also ensure legitimacy in the entire process. |

| 5 | Task delegation | 12 | 3 | 8 | Task delegation is considered to have low level of importance in the preimplementation phase because first legal know-how and communication should be undertaken and after that task delegation process should be encompassed. |

| 6 | Technological | 15 | 3 | 5 | Technological review of both firms is considered to have low level of importance in the pre-implementation phase because it depends on why the firm is undertaking the process of M&A and if M&A is not for the purpose of technological advancements, the technological review is not considered highly important. |

Good practice of During Implementation stage merging and acquisitions with the level of importance

The respondents were asked about choosing the level of importance for the good practices of during implementation stage of M&A given in the questionnaire. The respondents were asked to choose from the options such as low, medium and high. The responses are given below

| SR# | During Implementations | Level Of Importance | Justifications / note | ||

|---|---|---|---|---|---|

| Low | Medium | High | |||

| 1 | Socialisation | 1 | 16 | 6 | Socialisation is considered to have medium level of importance during implementation phase because with socialisation a certain interaction can be ensured between the employees of the merging firms as well as their management. |

| 2 | Cultural Adaptation | 2 | 3 | 18 | Cultural Adaptation is considered to have high level of importance during implementation phase because employees of both the firms will be able to adopt one single organisational culture and share similar morals and principles. |

| 3 | Value Preservation | 8 | 9 | 6 | Value Preservation is considered to have medium level of importance during implementation phase because value can be preserved once the firms are able to preserve organisational culture. |

| 4 | Good Governance of the M&A process | 5 | 2 | 16 | Good Governance of the M&A process is considered to have high level of importance during implementation phase because governance will ensure that all the employees and other stakeholders are governed with certain rules and given specific tasks in the M&A process. |

| 5 | Effective Communication | 8 | 10 | 5 | Effective Communication is considered to have medium level of importance during implementation phase because with communication the transparency can be significantly maintained. |

| 6 | Ensure disciplinary measures | 1 | 2 | 20 | Ensure disciplinary measures is considered to have high level of importance during implementation phase because it is highly important to have an authoritative body that ensures that all the functions are essentially and efficiently undertaken. |

The table above shows that out of all the respondents, 1 respondent has considered Socialisation as having low level importance whereas 16 have considered it to have medium level importance. Lastly, 6 have considered it to have high level importance. Moreover, 2 respondents have considered cultural adaptation as having low level importance whereas 3 have considered it to have medium level importance. Lastly, 18 have considered it to have high level importance. 8 respondents have considered value preservation as having low level importance whereas 9 have considered it to have medium level importance. Lastly, 6 have considered it to have high level importance.

For good governance of the M&A process, 5 respondents have considered it as having low level importance whereas 2 have considered it to have medium level importance. Lastly, 16 have considered it to have high level importance. For effective communication, 8 respondents have considered it as having low level importance whereas 10 have considered it to have medium level importance. Lastly, 5 have considered it to have high level importance. For the factor of ensuring disciplinary measures, 1 respondent have considered it as having low level importance whereas 2 have considered it to have medium level importance. Lastly, 2 have considered it to have high level importance.

Good practice of Post Implementation stage merging and acquisitions with the level of importance

The respondents were asked about choosing the level of importance for the good practices of post-implementation stage of M&A given in the questionnaire. The respondents were asked to choose from the options such as low, medium and high. The responses are given below

| SR# | During Implementations | Level Of Importance | Justifications / note | ||

|---|---|---|---|---|---|

| Low | Medium | High | |||

| 1 | Value Realisation amongst departments | 8 | 10 | 5 | Value Realisation amongst departments is considered to have medium level of importance in postimplementation phase because first it is important to focus on organisational culture and significant financial performance of the firm. |

| 2 | Asset reassessments | 2 | 3 | 18 | Asset reassessments are considered to have high level of importance in postimplementation phase because it will monitor the overall financial performance even after the M&A process. |

| 3 | Transition of operations, departments, mission and vision of the firm | 1 | 16 | 6 | Transition of operations, departments, mission and vision of the firm is considered to have medium level of importance in post-implementation phase because it will ensure as well as monitor that the firm has achieve all its objectives of M&A including transition of operations, departments, mission and vision. |

| 4 | Transformation of merged business | 8 | 9 | 6 | Transformation of merged business is considered to have medium level of importance in post-implementation phase because it will ensure that the objectives of business transformation are achieved at the end of M&A process. |

| 5 | Leading all stakeholders to common goal the a | 1 | 2 | 20 | Leading all the stakeholders to a common goal is considered to have high level of importance in postimplementation phase because it is highly important for the firm to keep the stakeholders at one platform in order to ensure that the financial, corporate and organisational strategic objectives related with M&A are accomplished. |

| 6 | Monitoring the progress | 3 | 4 | 16 | Monitoring the progress is considered to have high level of importance in post-implementation phase because monitoring will ensure that the entire process is undertaken prudently, the team has worked effectively and negotiations have brought significant results for all the parties to the M&A. |

The table above shows that out of all the respondents, 8 respondents have considered value realisation amongst departments as having low level importance whereas 10 have considered it to have medium level importance. Lastly, 5 have considered it to have high level importance. Moreover, 2 respondents have considered asset reassessments as having low level importance whereas 3 have considered it to have medium level importance. Lastly, 18 have considered it to have high level importance. 1 respondent has considered transition of operations, departments, mission and vision of the firm as having low level importance whereas 16 have considered it to have medium level importance. Lastly, 6 have considered it to have high level importance.

For transformation of merged business, 8 respondents have considered it as having low level importance whereas 9 have considered it to have medium level importance. Lastly, 6 have considered it to have high level importance. For leading all the stakeholders to a common goal, 1 respondent has considered it as having low level importance whereas 2 have considered it to have medium level importance. Lastly, 20 have considered it to have high level importance. For monitoring the progress, 3 respondents have considered it as having low level importance whereas 4 have considered it to have medium level importance. Lastly, 16 have considered it to have high level importance.

Feedback and Suggestions

Interviews using semi-structured questions had taken place in order to gain a broader detail and understanding of the topic. As per the collected responses it was understood that the chosen respondents were clear of the terms merger and acquisitions which subsequently had developed an ease for the researcher to obtain information regarding the questions of the questionnaire. The respondents were keen on supporting the decision that had taken place regarding the merger and acquisition of the case of FAB. They insisted that it was a joint effort of both the firms to share their investment and knowledge to develop a high performing organisation. It enabled to form a single venture and to gain a higher market share thus gaining more number of customers and shareholder value.

The action of merger and acquisition had further allowed to develop high amount of expertise in the organisation where two companies are now working under the same umbrella with the same goals and targets to be achieved. Respondents were diligent on replying whether the organisation they worked for had a strategy that supports mergers and acquisition and hence majority of them had a positive response which represents that the strategic is decision is highly favourable. As evaluated from the responses it can be understood that companies have acquisition strategies as well which they can use anytime they want. The results have also highlighted that employees alike managers also have a huge responsibility in the role of mergers and acquisitions where they are required to maintain certain operations in order to ensure that the strategy does not fail.

Another important aspect that was identified was that the respondents were also engaged in the action of forecasting in the directive to identify if the strategic decision of merger and acquisition had been beneficial. More importantly both the organisations are required to be align their expertise in order to develop financial dominion and to prove themselves as an effective corporation. It can be evaluated from the collected response that it is also the duty of the managers to communicate the organisational goals to their employees so a successful merger and acquisition can be maintained. Taking the case of FAB, communication is important since two firms of the same business operations have joined hands to achieve one single target. The individuals also feel that before taking the strategic decision of merging and acquisitioning it is important for both companies to inspect the financial performance of each other.

Managers are likely responsible to take full authority when establishing acquisitions so that they are no hindrances in the process and that if any issue occurs it is resolved immediately. It is also the duty of the mangers to assign respective roles to their subordinates to reduce any risks and uncertainties. The removal of uncertainties can potentially be beneficial to the functions of the firms and to strive for financial excellence. As per the responses it is highly essential that after the merger and acquisition the firms try to achieve their long term vision; however, its role is supposedly different in every company. The respondents consider merging to be highly beneficial for an organisation that can help in tackling external complexities and gain competitiveness.

Conclusion

This chapter has conducted a discussion of the merger and acquisition by taking the case of FAB.

A qualitative survey had taken place with the managers and employees that have been working

in the organisations through which it was important to get an insight of that their perspective was regarding mergers and acquisitions. It is therefore important to highlight that at first demographics have been shared in the study which include the age, gender, education and the level of education that the respondents have received. A total of 23 respondents had been chosen in the study in order to explore the concept of mergers and acquisitions. The view of respondents regarding the role of merging and strategies of acquisitions has been provided which entails that they consider it to be a very important and ideal strategic decision that can be taken by the upper management. Moreover risks related to it have also been discussed in order to understand the potential challenges that managers could face.

Discussion

In previous chapter, results of interviews are presented and the purpose of this chapter is to critically analyse the results using evidence from past studies. Primarily, the discussion below is aimed to show how each of the research questions have been answered by discussing the results obtained from interviews and comparison with past studies. This chapter is organised in a way to achieve this purpose. The chapter begins with discussion of drivers and benefits of M&A followed by discussion of challenges and barriers. Critical success factors and failure factors have also been discussed. The second part of the chapter presents discussion of good practices in three main phases of M&A implementation. Each of the practices identified in literature has been discussed in comparison with evidence provided in past literature. The third and final part of this chapter discusses the development framework. The development framework summarises the results and reorganises the evidence to show how development framework for M&A in banks has been developed in this study. The chapter ends with a small summary.

The first research question of this study was to analyse how decisions are made to adopt and implement merging in banking organisations. Within this content the researcher conducted interviews and asked respondents to show their opinions of about the term mergers and acquisitions. The results showed that mergers are considered to be combination or aggregation of resources and operations by two or more organisations to form one single entity to increase market share, add value to firms, and increase shareholders’ wealth.

Similar conclusions have be obtained from general literature. According to Ombaka and Jagongo, (2018) mergers and acquisitions involve the union of two or more independent companies and, up to that time, operated separately, so that they become jointly controlled firms. However, the distinction between the two operations is, in many cases, unclear. A merger is normally defined as a transaction where a company is combined with others, and in which the initial entities lose their identity. However, Greve and Man Zhang, (2017) differentiate mergers from acquisitions and defined the latter as a term which is classified as a transaction where a company acquires a stake in another company without combining the assets of both. On the other hand, a partial acquisition is similar to an acquisition but in which no real and effective control is established. Normally it usually implies some kind of cooperation, although it can also serve as a preliminary step for a future takeover.

The literature also showed that there are alternates to M&A activities or transactions called the strategic alliances which are defined as consolidation of operations which allows companies to collaborate without losing control. There are also strategic alliances that are associations between independent companies in certain activities, services or products. A joint venture is an agreement whereby two or more legally independent companies decide to create a company with its own legal entity but whose legal domain corresponds to them. This agreement generally leads to the creation of an entity in order to develop a common activity that will enjoy the technical and financial support of its members.

Furthermore, the results showed that interviewees agreed that there are strategic motives behind M&A transactions. It was observed that M&A are aimed to achieve for development and growth of the business in the hopes that the firms will success in the acquisition of market and sales along with immediate savings and gain easier and convenient access new markets and customers. Similarly, Barbopoulos and Wilson, (2016) revealed that in the wake of financial crisis in 2008, tha banks had a very defensive strategic approach and the M&A activities were mainly focused on the subsistence of the main financial entities that suffered from liquidity problems and bankruptcy risk. Although during the years before the crisis M&A operations were aimed at gaining size, creating economies of scale and developing new businesses, in the following years those objectives moved to the background. The entities sought to strengthen their balance sheets, simplify their business models and compensate for the fall in profitability.

Furthermore, Joash and Njangiru, (2015) highlighted another aspect that impacted the banking sector in all its fields of action, and M&A decisions are no exception. This was the deep regulatory reforms that governments and regulatory bodies applied throughout the world. These had contradictory effects on the M&A. On the one hand, they were a discouragement for these operations because they try to control more the activity of the institutions in order to reduce the risk. In addition, the unpredictability of the reforms affected the ability of the entities to plan and undertake any FyA operation. However, on the other hand, regulations such as those of Basel III forced banks to strengthen their capital, which stimulated consolidation processes. In the US, a month after his arrival at the White House, Donald Trump proposed a series of transformations in the Dodd-Frank Law, which if they were to be accepted by Congress and then effectively materialized, would entail changes in the environment regulator of the financial sector that could influence M&A operations.

Furthermore, the results showed that employees and managers have a critical role to play in M&A process. The results showed that in case of mergers the main roles include forecasting the effects of merger on assets, market share and shareholder value. Furthermore, forecasting and predicting the effects on firm efficiencies and control on its financial and corporate level. Furthermore, the managers opined that they are to communicate the aims and objectives of mergers along with motivating the work force and corporate governance. Similar roles were identified in case of acquisitions (see section 5.3.5, 5.3.6 and 5.3.7).

The literature search shows that the results above have also been cited in past literature. For example, Rozen-Bakher, (2018) argued that M&A are very important strategic decisions and these activities are based on works of many employees and not only the decisions of higher management. Significant amount of work is performed before undertaking M&A activities. Managers conduct through analysis of potential growth that the firm can achieve from M&A activities in terms of market share, increase in customer base and increase in profitability.

Furthermore, Kyriazopoulos and Drymbetas, (2015) argued that accounting analyses are critical for the decision of M&A activities. The study stressed that although acquisitions are not as simple investment decision as investment in machinery or technology and therefore accounting analyses are performed to predict the impacts of acquisitions. Furthermore, synergies are critical for the success of acquisition and thus people at various level of organisational hierarchy are involved to assess possible synergies to be achieved through acquisition.

Furthermore, Brooks, Chen, and Zeng, (2018) posited that before M&A decisions are made there are three focus areas of pre-M&A analyses. The first is the determination of the value of the target company. The second is the determination of the maximum purchase price to be satisfied, and the third is the choice of sources of finance (particularly in case of acquisitions).

Chu, Teng, and Lee, (2016) focused on the pre-M&A activities and argued that the important aspect, as a reference for the subsequent negotiation of the merger is the exchange ratio or the purchase price in acquisitions. For this purpose, a varied group of techniques aimed at obtaining the value of the target company has been developed. Although, there is no universally agreed method and therefore the study recommended the joint use of all or some of them. It must be clarified that the final purchase price does not have to be known. Since the fixation of that value is surrounded by a series of factors such as the characteristics of the target company, the circumstances of buyers and sellers and the time chosen for the operation, depending on the general economic situation In this way, issues such as obtaining a commercial name, the concurrence of two or more purchase offers, the interest in penetrating safely in an unknown market, etc., are elements that will influence the value and price of different quantities.

According to Pohl and Tortella, (2017) it is critical to assess and refer to the similarity of operations. It is about identifying similar operations that have taken place in the recent past, although the main problem is obtaining accurate information about them, since some firms being private would have published financial and operational data into public. Furthermore, the manager also need to address the problem of comparability, since in many cases, the circumstances and singularities of the target company will be different from previous transactions. This does not prevent M&A through it is still a valuable reference, as it is indicative of the trend of mergers and acquisitions and the long-term strategic approaches of the companies. It is convenient to estimate the relationship between the market price of these companies and their book value to predict the market value of the target company.

According to Du and Sim, (2016) the most critical success factor in M&A is the achievement of synergies. Possibly synergies are the most commonly pointed motive as motivation for two companies to merge, but on many occasions, the concept of excessively broad meaning is endowed. If two companies can generate more value for their respective shareholders by operating together than separately, it is understood that there are synergies. DePamphilis, (2019) argued that managers must conduct through analyses of synergies in terms of operational synergies and financial synergies. Operational synergies are obtained through economies of scale and economies of scope. However, the benefit is not automatic, but its effectiveness will depend on the talent and skill of managers. Economies of scale consist of the distribution of fixed costs among a larger total production, so that the unit fixed cost will decrease as total production increases. Fixed costs are understood as those that cannot be altered in the short term, such as depreciation and depreciation costs, interest, workers’ base salary or union costs.

The main drivers for M&A identified in results of the interviews include, synergies, growth and diversification, and economies of scale for cost efficiency (section 5.3.8). Similar divers have been cited in literature which show that there is consistency between results of this study and past literature. Daniya, Onotu, and Abdulrahaman, (2016) focused on synergies as driver of M&A and posited that synergies can come from economies of scope, which consist in producing more, with the same resources, through the efficient use of those that were available. For example, Procter & Gamble uses its advanced marketing system to cover most of the personal care and pharmaceutical products market.

In case of diversification driven M&A, Casu, et al. (2016) argued that diversification refers to the decision of a company to leave its main markets, geographic and products, and lines of business, to enter other. The purpose of diversification is to utilize the financial resources obtained from existing markets and invest in other markets to increase profitability. However, Johan, (2019) classified all the motives under one umbrella term, value generation, and concluded that principle of value generation states that companies generate value by investing the capital they obtain from their investors, to generate future cash flows at a rate of return higher than the cost of capital. The faster the generation of income, and the more attractive the rate of return, the greater the value will be generated. For this process to be sustainable over time, the company must find a competitive advantage that will last and be defended against its competitors. M&A activities are more than often focused on achieving economies of scale. Economies of scale consist of the distribution of fixed costs among a larger total production, so that the unit fixed cost will decrease as total production increases. Fixed costs are understood as those that cannot be altered in the short term, such as depreciation and depreciation costs, interest, workers’ base salary or union costs.

The results showed that various benefits are obtained from M&A activities which include diversification, strategic realignment, economies of scale, increase in market power (section 5.4.1). In case of benefits cited in past studies, similar results are reported. For example, Frankel and Forman, (2017) concluded that diversification is considered to be very beneficial for merging companies. Two companies with a presence in radically different markets can be integrated in search of this objective. There are two arguments that justify the diversification of a company, reduce shareholder risk and take advantage of the opportunities offered by sectors with greater growth potential than the markets in which the company is currently located. Through diversification, the company will have a more stable income, since it will not depend on a single market. The lower the correlation between the cash flows of the entities, the greater the reduction in the volatility of the investment. The direct consequence will be greater confidence in the company by investors and financial institutions, which will mean a decrease in the cost of capital.

Within the context of strategic realignment, Halkos, Matousek, and Tzeremes, (2016) opined that business environments change rapidly in many aspects, but legal and technological dimensions are especially important, because they are factors that can lead a company to lose the right to act in a market due to regulatory change or to be very behind its competitors, if it is not possible to adapt to technological advances. M&A can help banks adapt extremely quickly to these changes in the environment. Although authors such as Micu and Micu, (2016) point out that this is a more proper motive for divestments, this was one of the factors that drove the wave of mergers of the 90s in the United States.

In case of risks identified in M&A activities, the results showed that the main risks identified by research participants are conflicts between merging workforce leading to demotivation and disappointment causing loss of human resources (section 5.4.2). Natocheeva, et al., (2017) reported a comprehensive list of risks associated with M&A activities which include risks identified in results as well as others. The study reported that less than half of the mergers are successful in accordance with the opinions of shareholders, customers and employees, the three groups to which the author gives greater value. The biggest risk that exists in a merger is to pay a premium above the real value of the target. To avoid this, a valuation of the individually considered entity and a measurement of the value of the combined entity resulting from the operation will have to be carried out. In both cases, it will be necessary to estimate the cash flows and the cost of capital to be discounted in the DFC in order to make a proper valuation.

Wanke, et al. (2016) also referred to cultural conflicts and impacts on employees and executives using the term corporate integration. The author stressed upon the elaboration of a pre-merger integration plan and the precise definition of the roles of each person. However, there may be some reluctance to follow it strictly by managers, who, ultimately, are responsible for implementing it. On many occasions this is the reason why mergers fail. On the contrary, the excessively strict implementation of the plan could also frustrate the operation because, in any case, it will be necessary to adapt to the changes in the environment and to the reactions of the stakeholders, which cannot be foreseen with total accuracy. The predisposition of managers and workers, business culture and informal organization play an essential role.

The results found that main barriers and challenges faced by the M&A activities in banking industry include lack of communication, employee retention and cultural challenges as some of the major factors (see section 5.4.4). Similar barriers have been identified in past literature. According to Karolyi and Taboada, (2015) conflict of interest between merging parties is particularly an important challenge. The conflict of interest and lack of agreement between merging companies is a significant threat to success of merger. This is particularly an important element in case of hostile takeovers where the firm being acquired is not satisfied with the transaction. The main outcome of conflict of interest, if realised leads to differences and struggles between managements and thus negatively affects smooth transition.

Furthermore, Angwin, et al. (2016) stressed upon the use of proper change management framework during M&A activities as a solution to eliminate various problems such as lack of motivation, hostile reaction by employees under the fears and uncertainty of what would happen to them after the acquisition and other factors. The study recommended that proper communication channels and systems are aimed to engage employees and address their issues and concerns during and after the mergers. The most commonly cited agenda of communication is to address any issue of employees in terms of job security and aimed to elaborate on individual benefits of M&A.

As per the results reported in section 5.4.5 the main success factors identified by the banking sectors employees include trust between managements of merging organisations, resistance towards the change, and experience with previous mergers. However, the literature review showed quite a large list of success factors that are relatively different from the factors identified in the interview results. Within the context of banking industry, Howson, (2017) identified that due diligence is one of the most important critical success factors. Due diligence refers to the investigation and integral diagnosis which refers to carrying out in detail a series of small audits on financial, fiscal, human resources, trade union, legal and operational aspects of a company.

The idea is to make sure that there is significant and lucrative potential for M&A activities.

Furthermore, Ozturk, (2016) also identified a variety of critical success factors and stressed upon the degree of the strategic product-market integration. This refers to the degree of adapting the portfolio of products of the acquired by the bank to the objectives and strategy of the acquiring bank to be competitive and cover most of the market in which it operates. The study also highlighted the importance of the operational integration that involves integrating processes, production lines, technology, patents, complementing resources between both companies; on the one hand the acquiree, and on the other, the acquirer. Furthermore, Adeleke, et al. (2019) stressed upon the financial integration, which has to do with adapting the financial systems of the acquired company with the financial systems of the acquiring company, in order to make money management efficient and maximize the value of the company. In addition the integration of human capital, which is related to managing the capacities, attitudes, skills and knowledge of each of the people of both companies involved in the acquisition process, with the purpose of optimizing their productive work.

In case of failure factors, the results in section 5.4.6 showed that main failure factors identified are lack of involvement of the owners, difference between theoretical and practical valuation, lack of clarity, cultural integration issues and negotiation errors. It can be observed that these factors are the other side of the coin of critical success factors. Each of these factors relate to lack of integration in one or more aspects. Comparing these to previous literature Lee and Carter, (2018) reported that one of the main factors of failure of M&A is lack of integration and compliance. The product-market synergy is very important and lack of which creates significant problems for the firm after the M&A. The product-market synergy refers to the different product-market combinations that are defined as the company’s strategic business units. In this regard there are as many areas as possible missions (target markets) that the company can combine. If these are not obtained the value creation principle as discussed above is compromised and objectives of M&A are not achieved.-

Hamza, Sghaier, and Thraya, (2016) posited that lack of operational synergy which refers to collaboration so that the sum of the joint operational efforts of the companies involved in the merger operation is greater than the sum of the individual efforts is the main failure factor. The study justified this assertion by arguing that if M&A fails to provide profitable opportunities to individual companies as compared to those that each of them were obtaining before the M&A, then it becomes the main failure factor. The lack of financial synergy is also an important and commonly cited failure factor in past literature. Financial synergy consists in increasing the value of the merged companies created by strictly financial advantages linked to mergers and removals, which cannot be achieved by private investors through the private management of their portfolio of shares. The assimilated culture represented by the degree to which the organizational culture of both companies achieves shared values among their members, an aspect that distinguishes one organization from others.

In this section, this study compares the results regarding implementation of M&A strategy through comparison with past literature. The first factor identified in the results was strategic Planning and the results showed that strategic has a high importance in the pre-implementation phase. This is based on the rationale that the M&A activity is a major business decision which affects current and future state and wellbeing of the firm and therefore through strategic planning is required to ensure smooth transaction.

Within this context, Ahdizia, Masyita, and Sutisna, (2018) argued that the foremost aspect of strategic planning for M&A is to conduct due diligence. Due diligence implies the analysis and evaluation of all the key elements that influence the decision to proceed with M&A. It may be a legal obligation, but the term is commonly more applicable to voluntary investigations. A structured process requires a series of studies that help confirm the impact of business M&A. This is of great help to corporate directors and serves as a shield or shield against possible counter-arguments, debates, and even lawsuits promoted during and after the transaction. It is also required by sellers to ensure that buyers have all the elements to consider the value of the transaction. Considering its importance, Due Diligence reports should be entrusted to prestigious specialists with experience in the field. At this point it is important to reiterate that due diligence was also found as one of the critical success factors in discussion presented in section 6.2.5.

The second good practice identified in the pre-M&A implementation phase is communication of objectives. The results showed that communication of objectives is a medium level important factor in the pre-M&A phase. In this practice M&A leaders must communicate with the stakeholders including employees of the firms and explain them the rationale and benefits behind M&A and motivate them to support and play their role in the M&A process.

Similar conclusions have been found in Sarala, Vaara, and Junni, (2017) who argued that the role of stakeholders is critical for the success of M&A and for any other organisational strategy or organisational change for that matter. The study reported that there diverse stakeholders are involved in M&A process among which employees and shareholders are most critical along with regulatory authorities who keep string watch on M&A transactions in the economy.

These results can be related to previous results in which it was established that value creation is the main motive for any M&A activity and according to the value creation principle the purpose of increasing the wealth of shareholders is to gain satisfaction and increase the investment potential of the firm. However, it is also important to note that it has been established that lack of integration of human factor such conflict of interest among employees and management of companies involved in M&A is a critical failure factor. Therefore this study concludes stakeholder communication is critical in pre-M&A phase.