- Dissertation Topics (185)

- Accounting Dissertation Topics (8)

- Banking & Finance Dissertation Topics (10)

- Business Management Dissertation Topics (35)

- Economic Dissertation Topics (1)

- Education Dissertation Topics (12)

- Engineering Dissertation Topics (9)

- English Literature Dissertation Topics (3)

- HRM Dissertation Topics (3)

- Law Dissertation Topics (13)

- Marketing Dissertation Topics (9)

- Medical Dissertation Topics (7)

- Nursing Dissertation Topics (10)

- Other Topics (10)

- Supply Chain Dissertation Topics (2)

- Research Topics (16)

- Biomedical Science (1)

- Business Management Research Topics (1)

- Computer Science Research Topics (1)

- Criminology Research Topics (1)

- Economics Research Topics (1)

- Google Scholar Research Topics (1)

- HR Research Topics (1)

- Law Research Topics (1)

- Management Research Topics (1)

- Marketing Research Topics (1)

- MBA Research Topics (1)

- Medical Research Topics (1)

- Guide (63)

- How To (33)

- List (20)

IMPACT OF DIVIDEND POLICY ON SHAREHOLDERS WEALTH AND FIRM PERFORMANCE IN UK LISTED FIRMS

[Name of Writer]

[Date of Submission]

Table of Contents

INTRODUCTION

Background

Acharya et al., (2011) explain that dividend amount constitute a shift from recipient to shareholders in breach of the preference of debt on equity. Mehta (2012) states that the prime component of corporate principle is the dividend payment plan of an organization. Dividend is the payment that organization gives to their shareholders against their investment and risk; dividend payout policy is decided by various guidelines within an organization. Subsequently, guidelines or elements consist of limitation of financing, options for investment and selection, company size, enforcement from shareholders and managerial authorities. On the other hand, dividend policy does not comprise of amount paid to shareholders but it also consist of the information regarding organization’s recent progress and future prospects (Ajanthan 2013).

Gul et al. (2012) determine that the policy due to which there is rise in stock price of organization which in return accelerate shareholders prosperity is known as optimal dividend policy. Although, the link between dividend policy and wealth of shareholders remains mystifying. The acceleration of shareholders wealth is the prime focus of organizational principles, which in return increases value of organization which is calculated through organization’s common stock value. Therefore, to accomplish the objectives set by company executives, they should consider providing shareholders an equitable amount on their financing. The share price of organization in market is denoted by shareholders wealth which measures performance of funding, financing and dividend payout options of an organization. Dividend payout policy of organization have consequences for many stakeholders consisting of employees, investors, lenders, government and others. The dividend policy provides a measure through which shareholders determine the value of the company and predict their return on investment, dividend for shareholders is considered to be an income generating source even if it is finalized today or later in future.

Problem Statement

According to Adediran and Alade (2013) investigate that there is association of dividend pay-out method and firm execution in area of profitable investment which improves earning per share of the company. Majority of the studies are conducted to explore this relationship whereas, researchers concluded that earning per share and dividend payout are two different perspectives which should be taken into consideration on one on one basis so that desired efficiency and profitability can be attained. Al-Haddad et al. (2011) consider that these results cannot be imposed on developing countries. But various studies have concluded that operating cash flow and profitability have significant impact on one another but there has been insignificant relationship with ownership, cash flow responsiveness, size and resistance, (Afzal & Mirza, 2010).

Despite all the theories, dividend payout policy have been analysed with various variables in order to understand the dividend policy nature but not a single appropriate statement has been found which can conclude the definite result on dividend payout of companies, (Agyei & Marfo- Yiadom, 2011). However, the dividend payout policy influence on shareholders wealth and its’ impact on firms performance will be evaluated considering UK listed companies to have an insight of dividend policy effect on these variables. Majority of the studies have been conducted on developing countries perspective due to which the purpose of this study is to explore the impact of dividend policy on developed country’s firm performance and shareholders wealth.

Research Objective

- To understand the conceptual significance of dividend policy and shareholders wealth

- To determine the factors of dividend policy that influences shareholders wealth and firm performance

- To identify the impact of dividend policy on shareholder’s wealth and firm performance in UK listed firms.

- To provide set of recommendations for firms to increase dividend distribution for shareholder’s in order to increase firm performance.

Research Question

- What is the impact of dividend policy on shareholders wealth in context of UK listed firms?

- What are the factors of dividend policy that affect shareholders wealth?

Rationale and scope of research

Ouma (2012) determines that firms’ earning is an indicator which demonstrate whether the performance of firm is profitable or not. The dividend payment is the amount that company pays to their shareholders against their investment and risk so to determine whether the company is profitable enough or not shareholders consider it as an important aspect while deciding about investment in the firm. Shareholders evaluate the earning being generated by firm and dividend they pay to their shareholders, due to which the study emphasises on considering what role does dividend policy performs in increasing shareholders wealth and enhance firms’ performance in terms of companies listed in UK as well as the importance of dividend payout policy in firms’ perspective. asically the focus is to identify the approach through which organizations can formulate dividend policy which is in best interest of shareholder to gain their trust and commitment with organization and based on dividend policy improve firms’ performance.

LITERATURE REVIEW

Impact of dividend policy on shareholders wealth

AsmaTahir (2014) investigates the factors of dividend payout consist of payout ratio, book value to market value and price earnings ratio and its effects on wealth of shareholders. The executives have to decide based on the current situation of the business while formulating dividend policy and financial policies which aid in the process of attaining organizational goals. Though, profit remains the focal point as it is the prime source through which organizations are recognized on dual leading positions. First, profit can be retained for the future growth and expansion of firm and secondly it can be preserved for dividends of investors. Other than that, it can be used for payment to shareholders or buy back the shares of organization which are distributed in the market. Hence, the study indicated that it depends on executives strategy regarding dividend payment policy in which they decide to issue dividend payments to shareholders or not and if yes then determine the amount, (Farrukh et al., 2017). It was determined from the same study that the dividend policy is termed to an important aspect for company because it indicates the stability and communicates details of future projects of organizational expansion.

Various studies have highlighted the areas in which finance managers and investors have conflicting point of view. The reason is because executives’ interest contradicts with investors’ interest on the basis of different responsibility as executives have to plan strategy for increasing shareholders wealth and for the growth of business. The problem arises when there is abundant cashflow within the company and executives decide to use for expansion purpose of organization besides paying premium to investors. Shareholders have to analyse company performance based on executives decisions critically and amount serve on analysing executives decision is consider as agency cost because dividend payment is seen as a factor to reduce agency cost, (Ong et al., 2014). Chaabouni (2017) identifies that the dividend payment are the indicators which communicate details of future decisions of company .When the company declares dividend amount it eventually effects firms’ stock prices, dividend amount determines the performance of company in terms of liquidity. According to Hasan et al. (2013) consider that when organization reduce the dividend amount is impacts company position adversely which results in decrease in stock prices.

Thus, executives develop appropriate strategy within which they decide the amount to be distributed among shareholders and the amount to be kept for retained earnings of the company. Retained earnings are the main component through which a company invest in those areas where they can achieve prosperity in corporate world, (Bawa & Kaur, 2013). Corporate growth or expansion is consider to be the element through which they can increase the amount of dividend paid to shareholder. The company market value of shares is determined by the amount of dividend paid by company, the Bawa and Kaur (2013) state that investors consider dividend as future source of earning so for them dividend is the vital element which plays an important role in investors wealth.

Research Instrument

Research instrument suggests that using a specific method of data collection, how the data has been gathered by the researcher. Since the researcher has adopted a secondary method of data collection, therefore the data is collected through various sources which include books, articles, journals, websites and annual reports of the companies. The data related to macroeconomic factor has been gathered from the annual global competitiveness report which is published by the World Economic Forum. Moreover, the data which is related to the automotive sector of Pakistan has been gathered from the annual reports of the listed companies. In this manner, the data has been gathered by the researcher for the purpose of conducting this study. The financial data has been collected from the financial reports of the company for the period of 10 years.

Impact of dividend policy on firms’ performance

According to Agyei and Marfo- Yiadom (2011) it was evaluated that the shareholders when investing determine dividend payout policy of the company on the level of risk involved, profitability, ownership formation, cashflow and taxation as key elements because these are the aspects which influence shareholders payment. Various studies have been conducted on significance and insignificance of dividend payout strategy. The study considers that market fluctuation, lacking of correspondence, development cost, taxes, operating leverage cost, costs of securities and behavioral elements should be determined when evaluating effect of dividends on company value.

Subsequently, there are less chances for any country to consider perfect market economy but if perfect economy is taken into consideration the dividend policy will still be the most important aspect. The firms who pay dividend are determined to be more profitable, involve less risk, secure and developed comparative to those firms who don’t pay dividend. Additionally, the impact of dividend remains a controversial aspect for concluding firms performance because the amount of dividend can’t be fully determine the company execution due to difference in market they operate, stable situation of economy and other macroeconomic factors.

Jiraporn et al. (2011) assess that dividends play an important role for raising capital externally for future investments which led to improve firm performance as well as broadens the extend on which external regulatory bodies observe company performance in capital market. This raises the standard of corporate governance regulations which significantly impacts execution of firm. Ouma (2012) explores that firm performance is enhanced by paying investors on their investment in a positive manner and accepts the participation of dividend payout in improving company’s performance as well as it contradicts those theories which consider dividend payment plan as unconnected and supports the results of Jirapon et al. (2011). Although, not only dividend payment plan but overall assets of company and revenue generated by company are also the key factors in determining an organizations performance according to the study.

Conceptual framework

The conceptual framework of this study represents variables which are dividend, shareholders wealth and company performance. The dependent variable is dividend policy and shareholders wealth and company performance are independent variables. This study analyses the impact of dividend on shareholders wealth and company performance.

Hypothesis

H0: There is no significant impact of dividend yield on shareholder wealth and company performance

H1: There is significant impact of dividend yield on shareholder wealth and company performance

RESEARCH METHODOLOGY

Research Philosophy

Matthews and Ross (2014) refer research philosophy as a conviction or assurance on which the study is being conducted. This area is the vital aspect of research as within it information is collect according to the need of the research topic. Research philosophy assist in the process of providing an authentic conclusion of the study on the purpose of which study is being conducted. Realism, positivism, interpretivism and pragmatism are known as research philosophies which are applied in various studies. Realism research philosophy is the school of thought in which researcher collects data through using general observation and this theory supports secondary data for which the knowledge of objectivity of human mind is the prime importance, (Bryman & Bell, 2014). Although, within the context of this study positivism research philosophy will be applied because the study is based on secondary data as the first hand data cannot be collected for this study, data of variables for this study will be collected through annual reports and UK data bank will be approached for this study.

Research Philosophy

Creswell (2013) considers that the research method as a systematic approach through research procedure can be defined. There are three types of research design which are qualitative, quantitative and mixed research method. Quantitative research methodology will be used in this study due to the fact that this study is based on the variables and data of these variables is in annual reports and in UK data bank, study is based on collection of economic data consisting of numerical data. Punch (2013) determines that the quantitative research method as evaluation of research dilemma through which the information is being converted into mathematical and arithmetic data.

Data Collection and Sample Size

Kumar (2010) determines that there are two types of data collection method named as qualitative and quantitative data collection. The data collection is a method through which the appropriate data for research or for the purpose of study is collected so that study can be summarized through authentic conclusion and evaluate data placed on sample size and to examine hypothesis with the collaboration of appropriate data, (Driscoll, 2011). Secondary data collection sources are various online and offline portals such as journals, research papers and others. Though, primary data are collected through questionnaire or conducting interviews. The data for this study will secondary form of data which will be collected through UK data bank, listed companies of UK data will be analysed for this research. The variables of this study are dividend, company performance and shareholders wealth all the data for these variables is in numerical form. Dividend pay-out ratio denoted the data of dividend, shareholders wealth is determined through net present value minus cost and company performance will be represented by profit earned by company all this data of variables will be collected through annual report of company due to which this approach is appropriate for this study.

Data Analysis Technique

Data is analysed in order to reach to a final conclusion and conclude the study with genuine results. The technique used in this study will be regression to explore correlation and determine issue of this research.

Ethical Consideration

The study has consider all the moral concerns that ought to be focused and gave careful consideration while conducting research and additionally guaranteed that any of their data will not be uncovered. After evaluating the information it will be disposed of and any further personal data was not asked from companies. The information would utilized for one and only legal reason that was communicated to the companies that it won’t be further transformed for another illegal purpose and it won’t be kept after completion of report rather it will be kept for the time that is obliged to have the companies information.

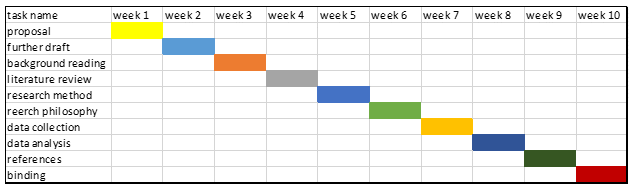

Gantt chart

References

Acharya, V.V., Gujral, I., Kulkarni, N. and Shin, H.S., 2011. Dividends and bank capital in the financial crisis of 2007-2009 (No. w16896). National Bureau of Economic Research.

Adediran, S.A. and Alade, S.O., 2013. Dividend policy and corporate performance in Nigeria. American journal of social and management sciences, 4(2), pp.71-77.

Afzal, T., Mirza, H., 2010 “Ownership Structure and Cash Flows as Determinants of Corporate Dividend Policy in Pakistan”, International Business Research, Vol. 3(3) p. 210-221.

Agyei, S.K. and Marfo-Yiadom, E., 2011. Dividend policy and bank performance in Ghana. International Journal of Economics and Finance, 3(4), p.202.

Ajanthan, A., 2013. The relationship between dividend payout and firm profitability: A study of listed hotels and restaurant companies in Sri Lanka. International Journal of Scientific and Research Publications, 3(6), pp.1-6.

Al-Haddad, W. et al. 2011. The effect of dividend policy stability on the performance of banking sector. International Journal of Humanities and Social Science, 5(1)

Al-Hasan, M. A., Asaduzzaman, M., & Karim, R. A. 2013. The effect of dividend policy on share price: An evaluative study. IOSR Journal of Economics and Finance, 1(4), 6–66.10.9790/5933

AsmaTahir, N.R., 2014. Impact of Dividend Policy Shareholder Wealth. Journal of Business and management, 16(1), pp.24-33.

Bawa, S.K. and Kaur, P., 2013. Impact of Dividend Policy on Shareholder’s Wealth: An Empirical Analysis of Indian Information Technology Sector. Asia-Pacific Finance and Accounting Review, 1(3), p.17.

Bryman, A. and Bell, E. 2014. Research methodology: Business and management contexts

Chaabouni, I. 2017. Impact of dividend announcement on stock return: A study on listed companies in the Saudi Arabia financial markets. International Journal of Information, Business and Management, 9(1), 37.

Creswell, J.W. 2013. Research design: Qualitative, quantitative, and mixed methods approaches. Sage publications.

Driscoll, D. L. 2011. Introduction to primary research: Observations, surveys, and interviews. Writing Spaces: Readings on Writing, 2, 153-174.

Farrukh, K., Irshad, S., Shams Khakwani, M., Ishaque, S. and Ansari, N.Y., 2017. Impact of dividend policy on shareholders wealth and firm performance in Pakistan. Cogent Business & Management, 4(1), p.1408208.

Gul, S., Sajid, M., Razzaq, N., Iqbal, M.F. and Khan, M.B., 2012. The relationship between dividend policy and shareholder’s wealth. Economics and Finance Review, 2(2), pp.55-59.

Jiraporn, P., Kim, J., & Kim, S. Y. 2011. Dividend payouts and corporate governance quality: an empirical investigation. The Financial Review, 46, 251 – 279.

Kumar, R. 2010 ‘Research Methodology: A Step-by-Step Guide for Beginners’, SAGE Publications Ltd; Third Edition

Matthews, B. and Ross, L. 2014. Research methods. Pearson Higher Ed.

Mehta, A., 2012. An empirical analysis of determinants of dividend policy-evidence from the UAE companies. Global review of accounting and finance, 3(1), pp.18-31.

Ong, A. S. K., Lim, A. S., Lim, M. Y., Ow, Y. P. Y., & Tan, L. L. 2014. The impact of dividend policy on shareholders’ wealth: Evidence on Malaysia’s listed food producer sector (Doctoral dissertation). UTAR.

Ouma, O.P., 2012. The relationship between dividend payout and firm performance: a study of listed companies in Kenya. European scientific journal, 8(9).

Punch, K.F. 2013. Introduction to social research: Quantitative and qualitative approaches. Sage.

View More Samples

WhatsApp Now

Get Instant 50% Discount on Live Chat!

WhatsApp Now

Get Instant 50% Discount on Live Chat!