- Dissertation Topics (185)

- Accounting Dissertation Topics (8)

- Banking & Finance Dissertation Topics (10)

- Business Management Dissertation Topics (35)

- Economic Dissertation Topics (1)

- Education Dissertation Topics (12)

- Engineering Dissertation Topics (9)

- English Literature Dissertation Topics (3)

- HRM Dissertation Topics (3)

- Law Dissertation Topics (13)

- Marketing Dissertation Topics (9)

- Medical Dissertation Topics (7)

- Nursing Dissertation Topics (10)

- Other Topics (10)

- Supply Chain Dissertation Topics (2)

- Research Topics (16)

- Biomedical Science (1)

- Business Management Research Topics (1)

- Computer Science Research Topics (1)

- Criminology Research Topics (1)

- Economics Research Topics (1)

- Google Scholar Research Topics (1)

- HR Research Topics (1)

- Law Research Topics (1)

- Management Research Topics (1)

- Marketing Research Topics (1)

- MBA Research Topics (1)

- Medical Research Topics (1)

- Guide (63)

- How To (32)

- List (20)

EVALUATION OF IMPACT OF SERVICE QUALITY ON CUSTOMER RETENTION: A CASE STUDY OF PAKISTANI COMMERCIAL BANKS

[Name of Writer]

[Date of Submission]

[Name of Institution]

Abstract

The underlying study intends to cover different aspects service quality and its relation with customer retention. In this regard, the objectives has been addressed in this study is based on highlighting the significance of service quality and customer retention and identifying the factors of service quality affecting the customer retention in commercial banks of Pakistan. The nature of the data for this study is mixed, thus the researcher have selected the quantitative and qualitative data together. The data used for this research consists of numeric figures and quantitative and qualitative data information being taken through the interviews. This research is based on first-hand collected data by the research in the form of surveys and interviews. The researcher has implemented the primary data collection method for this kind of study. In this study, the researcher has used SPSS in order to apply the relevant tests over the collected data. The findings of the study revealed that there is a positive association between service quality and customer retention in the commercial banking sector of Pakistan. Therefore, it was recommended that Employees of the banks should be allowed to go out of the box for solving the issues of customers following remaining in the boundaries of the policy.

Table of Contents

CHAPTER 1: INTRODUCTION

Background of Study

The current modernised age of rapid development and advancement has made the business environment highly complex and dynamic that has provided customers with numerous options in the market (George and Kumar, 2014). Customer retention, by increasing their satisfaction level, has become one of the major concerns for organisations because customers are considered as the drivers of the profitability and growth of the firm (Ngo and Nguyen, 2016). Rapid increase in competition and expansion of market has created the need for the organisations to emphasis over their service quality prospects that can contribute in obtaining customer loyalty and retention (Siddiqi, 2011). The term customer retention refers to the capability and potential of the organisation to retain or hold on it customers through products and services that can add value to the profitability and revenues of the firm (Ishaq, 2012). In this regard, factor of quality plays dominant part in enhancing the customer satisfaction level (Karim and Chowdhury, 2014). The study accumulated by Kasiri et al (2017) emphasised that customer retention and satisfaction are two interrelated concepts that trails each other. Customer satisfaction level can be defined as driver of the customer retention because when customers have the satisfactory experience with certain organisation it encourages them to acquire approach same organisation in future as well to obtain their services (Zameer et al, 2015). However, exceptional service quality standards is key to fuel the customer satisfaction level (Awan et al, 2011). In this underpinned study, in-depth discussion over different prospects pertaining to the effect of service quality on customer retention in commercial banks of Pakistan has been conducted.

It is evident that banking sector plays crucial in role development and stability of the economic conditions of the country (Ali and Raza, 2017). Firms operating in banking sector holds significant position in strengthening the financial market and the way money circulates in the country through effective banking system (McKecnie et al, 2011). Generally there are different types of banks operating Pakistan such as commercial banks, Islamic banks, central bank, microfinance, co-operative banks and specialised banks that tend to provide services to the people according to their objectives (Hafeez and Muhammad, 2012). Currently, there are 35 banks operating as commercial banks Pakistan (SBP, 2020). Banking industry of Pakistan is regulated and controlled by the parent node that is state bank of Pakistan that governs the local banks operating in the country under prudential regulations (Khan and Fasih, 2014). Commercial banks are considered as the financial institutions that offers different banking services to customer such as accepting account deposits, saving accounts and giving loans with the goal to earn the substantial amount of profits through interest (Kanwal and Nadeem, 2013). Askari, Bank Alfalah, Allied Bank limited, Citi Bank, Faysal Bank and Bank Al Habib are some of the major commercial banks that are operating different sectors such as public, private and foreign in Pakistan (Naeem, Akram and Saif, 2009)

Changes in dynamics of the world regarding the way system performs and tasks carried out has influenced the way people manage their finances and assets. In 2018, in Pakistan number of bank accounts reached to the 50 million that indicates the substantial reliance of customers over banking firms to manage and secure their finances (Yasir, 2020). However, people in Pakistan possess multiple options to obtain the commercial banking services due to the presence of different banks that are striving hard to deliver exceptional services that can attract the customers towards their firm increasing the profitability (Hafeez and Muhammad, 2012). The pursuit of service quality can be defined as the tool for the organisation operating financial sector to create the competitive advantage by up-scaling the prospects of their services that can help organisation to take lead in the dynamic industry (Siddiqi, 2011). However, in existing competitive environment, maintaining the top position is also the major concern that can be catered through massive customer demand in market. Profitability and stability of commercial banks heavily relies on the number of customers they have because these firms earns through interest and extra profits on services charged by customers (George and Kumar, 2014).

In banking sector, services is the on-going process where banking personnel are required to deal with the hundreds and thousands of customers on regular basis in an efficient manner that can enhance the customer satisfaction level (Al-Tit, 2015). In banking sector, metrics of quality of services relies on the data security, timely response, availability of services and behaviour of the banking staff towards customers (Khan and Fasih, 2014). However, metrics of quality and standards can be different for every organisation depending on the type of services provided by them and target audience. While relying over certain financial institutions, security is one of the imperative prospects that concerns the customers and influence their decision whether they should trust certain bank for their financial valuable or not (Vijay Anand, and Selvaraj, 2013).

Furthermore, rapid surge in usage of internet banking has increased the threat related to data security in banking. According to the News (2018), cyber security and cyber threats is one of the leading issue in banking sector of Pakistan that has affected the customer trust and satisfaction level towards their financial service providers in the negative way. Commercial banks are considered as the customer centric organisation where employees are required to directly deal with the customers and behave appropriately without discriminating among them on the basis of caste, creed, race, appearance, gender, religion and social background (Kasiri et al, 2017). Employees are considered as another imperative asset of organisation that play key role in keeping the organisation operational and add value to its productivity (Kaura and Datta, 2012). While dealing with customers directly, behaviour of employees holds great significance because any unethical or unsatisfactory attitude from employee can result in customer dissatisfaction (McKecnie et al, 2011).

Focusing over these minor aspects helps the organisations to strengthen to their quality of service and create positive perception among customers about their brand. The study by Albarq (2013) advocated that enhancement of customer satisfaction level is the continuous process practised by service oriented organisations because changes in customer expectations level up-scales their expectations level as well that influences the need to enhance the quality of services. Service quality can be considered directly proportional to the customer satisfaction because high standard quality service can help to create the positive perception among customer (Paul et al, 2016). Furthermore, in regard to attain the long-term loyalty and customer retention it is essential for banking firms to emphasis over practices pertaining to customer satisfaction (Liang et al, 2013). For this purpose, underpinned research study incorporates the in-depth details regarding the way service quality affects or influences the customer satisfaction in commercial banking sector of Pakistan.

Aims and Objectives

The underlying study intends to cover different aspects service quality and its relation with customer retention. In this regard, following aims and objectives has been addressed in this study:

- To highlight the significance of service quality and customer retention.

- To identify the factors of service quality affecting the retention of customer in commercial banks of Pakistan.

- To evaluate the impact of service quality on customer retention in commercial banks of Pakistan.

To draw the set of recommendations for the managers working in commercial banks of Pakistan to enhance their service quality.

Research Questions

This particular research contributed answering the following questions:

- What is the significance of service quality and customer retention?

- What are the essential factors of service quality that influences the customer retention in commercial banks of Pakistan?

- What is the impact of service quality on customer retention in commercial banks of Pakistan?

Research problem

The research accumulated by Shahzad and Rehman (2015) stated that in banking sector of Pakistan, massive growth and efficiencies has been observed with the passage of time that has made the financial sector of the country an imperative part for the economic prosperity. However, expansion of the financial sector and rise in competition has laid the local Pakistani banks operating in this particular industry to face cumulative pressure due to the invasion of the foreign commercial banks in the country such as Citi Bank, Industrial Commercial Bank of China limited (ICBC) and Deutsche bank AG (SBP, 2020). Furthermore, rise of competition and dynamic business environment has made the survival and growth of the local commercial banks of the Pakistan negatively.

Foreign commercial banks accumulating profits from people of Pakistan tends to invest in development and growth of their own economy rather than Pakistan economy (Haneef et al, 2012). Furthermore, with the help of strong technological assistance, financial resources and backup’s foreign commercial banks in Pakistan easily attracts the customers towards their organisation. Therefore, these issues and increasing competition in financial sector of Pakistan has created the needs for Pakistani commercial banks to emphasis over their quality standards that can contribute in increasing the customer satisfaction level resulting in obtaining customer retention. In this regard, the underpinned has contributed in addressing the problem by highlighting the way service quality can influence the customer retention in commercial banks of Pakistan that can help in increasing their profitability and market position.

Significance of study

The underpinned research can be highly significant for the management and directors of the Pakistani commercial banks to familiarise them regarding the way improvement service measures can enhance their profitability and contribute in customer satisfaction level. This particular research is imperative to highlight the significance of service quality and customer retention because it helped the banking sector to evolve once again and contribute in economic sustainability of the country. Furthermore, this particular study is highly significant for the government and authorities of Pakistan to familiarise them with the way invasion of foreign commercial banks in the country and their expansion in different regions of the state is threatening the stability of the local commercial banks that directly creating the negative impact on the financial sector of the country. Furthermore, this study is significant for ministries and state bank of Pakistan to draft new service quality standards and regulations that can contribute in attracting more customers that would directly add to the stability of economic position of the country.

Rationale of study

Efficient banking system holds imperative position in strengthening the economic conditions of the country because it concerns with the way money circulates within the system. Furthermore, banking is one of the crucial business sectors of Pakistan and source of income from thousands of employee. The rationale behind conducting the study over banking sector is to highlight the significance of customer retention and service quality in banking sector because slowdown of Pakistan economy has made the financial sector highly vulnerable (The News, 2020). If foreign commercial banks starts to expand its operations rapidly in Pakistan, it might affect the position of Pakistani commercial banks negatively effecting the stability of financial sector and economy of the country. Therefore, reason behind conducting the study over customer retention in relation service quality is to encourage the commercial banks in Pakistan to develop the best quality standards that can increase their customer base and become preferred commercial by people. Furthermore, most of the previous study have been conducted over the entire banking sector of Pakistan to examine their service and customer satisfaction. However, has contributed in bridging the gap by narrowing down the focus on commercial banks of Pakistan only.

Structure of Study

First chapter covers the introduction section that highlights details about background of study, objectives, research problem, significance and rationale. Next section of the research covers the literature review that includes the critical analysis, theoretical framework and conceptual framework. Third chapter in the study incorporates the discussion over research methodology and data collection methods adopted by the researcher in particular study. Fourth chapter highlights the analysis of data accumulated through different sources and detail objective vice discussion to ensure research problem and objectives has been addressed properly. Lastly, Fifth chapter covers the conclusions and recommendation section of the study including the brief summary of findings.

CHAPTER 2: LITERATURE REVIEW

Introduction

Quality of service has become the most important challenge for banking sector all over the world. Majority of the banks all over the world use service quality as their tool to retain their customers. Moreover, customers have also become very conscious of the service quality delivered by commercial banks (Ajmal et al., 2018). The research conducted by Sari et al. (2018) highlighted that now in this modern era, the challenge has been increased in the banking sector to sustain their competitive position in the service sector by providing excellent quality and services products to the consumers in all over the world, specifically in the developing countries. The acquiring cost of the consumers is much higher than the retaining cost for banks hence, retention is a major element in bank’s strategy. Moreover, the regular customers understand new products very quickly than new customers due to which regular customers buy more products that help banks in producing profits and providing bank with the competitive edge.

Furthermore, Khan and Fasih (2014) discussed that regular customer also indirectly promote the services of the bank to others that increase customer trust in the specific bank. In the industry of banking, the competition has been increased from the past decade in which several banks compete for customer retention and base. Approximately, the services of all banks are same and presented as duplicate products due to which customers are attracted through the name of the products due to which banks have been differentiating their products in the global world. Moreover, the price and quality of the products also matter a lot. Customer retention is the most essential and challenging tool that has been used in the majority of banks to sustain the competitive advantage and gain profit. The strategies and patterns have been changed in the Pakistan’s Banking Industry.

The banking sector has nowadays majorly focused on the working condition of banks from the last decade due to which, banks in Pakistan are focusing on some effective strategies and techniques of promoting to retain their consumers by accomplishing the requirements of consumers and maintain them as regular customer (Hafeez and Muhammad, 2012). This chapter highlights the importance of service quality for consumer retention, the banking sector of Pakistan has been taken as the case study of this research. This research not only identifies the importance but also analyse and recognise the features that affect the banking sector to service quality and customer retention.

Concept of Service quality

According to the research by Urban (2013), in general, the quality of service can be well-defined as the delivery system of service for positive output through customer retention, rising profits and developing a positive image in the competitive market. However, the quality of services is directly interlinked with customer retention and the perceived service quality by the customers. Moreover, it found that service quality is not only a term, it is a major factor that impacts positively or negatively on the profitability and performance of an organisation. The term service quality is combined with two different words “service” and “quality”, which majorly focuses on the quality of services available to the users. The word quality emphasise on the specification or standards the organisation promises by generating effective services within the organisation. As the innovation frequency has increased in the banking sector, it will ultimately upgrade the quality process of products.

Moreover, Zameer et al. (2015) highlighted in their research that the customer retention can be increased in the banking sector by increasing the quality of services and providing effective services to their customers. The quality services not only retains the customers in banks but also maintain the loyalty of customers which can benefit in promoting their products and services to other consumers through word of mouth. In the past decade, majority of the customers were not aware of the quality of services due to which majority of the banks did not focus on attracting customers through service quality. Now in this modern era, the awareness of service quality has been increased due to which it is challenging for the banks to design and plan the effective strategy for their customers which more standard quality services. The service quality can be organised by the proper management of employees within the organisation, specifically in banks so that employees can handle customers and fulfil their needs and requirements by providing them effective quality services.

Significance of Service Quality

A modern commercial professional environment is a period of the customers which considers the excellence of services as an important aspect of getting accomplishment in the competitive atmosphere of the business world. Though the improvement in quality of services not only improves the satisfaction level of customers but also helps in increasing the streams of revenue. According to the research conducted by Kaushik (2013), the quality of the service effects the customer’s intention with regards to their purchases. The basic component in the quality of services is loyalty that is followed by the tangibles, behaviour, as well as the convenience of the employees.

As per the research conducted by Ajmal, Khan, and Fatima (2018), there are four magnitudes of the service quality in the division of banking that are, behaviour, capability, tangibles, and suitability. To satisfy the customer, one has to provide better services while ensuring that there are tech-based security and protection along with the provision of quality information and loyal and user-friendly services. According to Adhikari and Nath (2014), the satisfaction of the consumers is a highly essential aspect with respect to attract or preserve sustainable relations with the customers, more specifically in the sector of banking. This thought-provoking perception lets the service sectors pay more heed on extensively providing quality that tends to impact the satisfaction level of the consumers in a positive way. It is noteworthy to know that if the banks tend to focus on the requirements of the customers and try to achieve their satisfaction level, then definitely, the customers can be sustainably retained.

Factors Affecting Service Quality

Following are the aspects which directly or indirectly impact the service quality,

Reliability

As per the study conducted by Hafeez and Muhammad (2012), the term reliability is well-defined as the capability to accomplish the services which are guaranteed or committed in a dependable and accurate manner. There are some of the measures which can be used for measuring the rate of reliability in the delivery of quality services. That includes the provision of the services which are promised, the dependability of managing and handling the services of the customers, the timely performance and deliverance of all the services and also, the maintenance of the records that are error free.

Responsiveness

The word responsiveness refers to the ability which a company has for providing an appropriate and suitable data or information to the customers when there is any troublesome situation. It is a factor that tends to maintain a mechanism that is required for handling the responses or returns and also in providing needful guarantees. It is basically a willingness to helping the customers and providing them the services which are easy and speedy. As per the research conducted by Awan, Bukhari and Iqbal (2011), there are some measures of responsiveness which include informing the customers about the start of the services, willingness to guide the customers and an attitude to quickly respond to the requests of the customers.

Assurance

Tangibility is the level to which the physical resources, equipment, and the get-up of the staff members or any individual are in an adequate manner. Service quality is also reliant on on the provision of the equipment as well as other resources. According to the research of Hassan et al., (2013), the providers of the services adhere to make their employees’ appearance remarkable and also ensure that the needful equipment is to be provided. This parameter measures the dependability of the customer on the quality of the most visible features.

Tangibles

Assurance is another factor that is about the knowledge as well as the consideration of the workforces and their ability of carrying trust as well as self-confidence. Ali and Raza (2017) have mentioned in their research that to measure the level of assurance while providing quality services to the consumers, it is essential that an employee should ensure its customers with confidence and make him feel safe and secure while doing transactions. Moreover, an employee has to be courteous constantly and also has to abide by his promise of providing quality ensured service.

Empathy

According to the study conducted by Zafar et al., (2012), the term empathy means to provide a gesture of care as well as provide attention to every individual or customer. There are ways of measuring empathy that are focused on the worker’s willingness to being polite and considerate through its consumers. The organisation tends to give equal but focused heed on their concerns, complaints or requests and also to understand their query so that it can be resolved at the convenience of customers.

Current Service Quality Trends in Banking Sector

Today in this modern and competitive world, the banking sector has been become the most important sector for all the population globally due to which the banking sector has designed some strategies to develop effective quality services and products that attract more and more customers and retain them for future (Chaudhry et al., 2016). However, according to the research conducted by Subashini (2016), the present trends of service quality developed the most interesting variable for all the banks. This is because technology has become the most necessary factor for the banking sector and it had to divert business from traditional banking sector to e-banking system. The majority of the banks conduct the survey and take feedback from their customers to improve the service quality from which, it came to know that customers need easy accessibility to transfer money from one place to another.

The research of Hussain et al., (2017), discussed that the current e-banking system has been become the most trending service in the entire world, specifically in Pakistan due to which the majority of the customers fulfil their requirements through the website or mobile application of their specific bank. Moreover, customers are also becoming satisfied through the e-banking system. This trend not only enhances the service quality but also increased customer retention because now people want to reduce their time in physically visiting banks for the transaction and other formalities. Ray and Ghosh (2014) highlighted that the technology of e-banking not only decrease their time of transaction but also increases the profit of banks in Pakistan and globally. However, as the competition increased in the e-banking system, several complexities have been developed among different banks in the competitive market. For this, banks are developing an innovative approach to maintain the competitive environment and become the leader of the market.

Moreover, Dar (2012) asserted that there is an important connection among innovation of technology and profit. As the cost of innovation increased, the cost of profit ultimately increased, which helped in increasing the loyalty of customers through service quality with different approaches. There are several features that affect the customer’s satisfaction, specifically in the electronic-banking system through easy convenience, accessibility, and privacy, etc. To improve the financial management system, currently banking industry of Pakistan has been developed proactive engagement. With the incorporation of advanced analytics, improved data and spread opportunities and channels, the financial institutions have been spreading and expanding their services according to the customer needs and satisfaction to maintain their retention. Husnain and Akhtar (2016) emphasised that the proactive trend in a financial institution means to update consumers through message delivery by the capability of SMS and by mobile banking. Moreover, banks get in touch with customers by interacting with customers through call or feedback form to analyse the performance of new services and their influence on customer satisfaction and retention. Furthermore, the banks also developed their new feedback services for their customers to provide some recommendations to their banks through which they can enhance their services, in which the majority of the customers take an active part so that services of banks can give effective benefit to the customers.

Conceptualising Customer Retention

According to Chahal and Dutta (2014), the majority of the banks spend their time, resources and energy to develop customer trust through establishing an effective approach according to needs and requirements of customers. Customer retention can be elaborate as the process of engaging current regular consumers to remain purchasing goods and services. The concept of customer retention is different from customer achievement because majority of the businesses use some specific techniques to retain their customers. Moreover, Santouridis and Veraki (2017) discussed that banks retain their customers by offering them insurance programs and other e-banking facilities through which they stay connected with their banks. The retention rates of the banks are totally dependent on the strategies that developed by banking sector for refraining them to switch to rivals. Loyalty of customers is the most essential feature that can sustain customer retention and the majority of banks follow customer loyalty approach through which they recognise the needs of customer’s need and manage them by developing a specific approach that benefits both customer and bank.

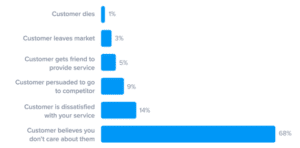

From the research of Chitra and Subashini (2013), it is asserted that banking sector maximises the profitability level by increasing customer retention through safe and secure services that develop the trust of customers. The picture given below shows the reasons why the customer leaves the bank. The consumer satisfaction and the attention of banks to their customers are the most two important factors that retain the customer in the banking sector. The figure below shows that approximately 68 percent of people leave the bank and switch to other banks because they did not get proper attention and treatment with their respective bank and 14 percent of people are not fulfilled with the excellence of the services of the bank due to which they left or switch bank.

Figure 1 Percentage and reason of customers for leaving bank

(Source: Chitra and Subashini, 2013)

Customer retention is the most essential element for the profitability of the banking system due to which it has become the challenge for every bank to develop effective strategies and approach to retain their customers specifically in developing countries like Pakistan (Fatima, and Razzaque, 2014).

Significance of Customer retention

Customer retention is necessary for getting the achievement in service businesses including the likes of banks. The service quality is a significant feature in the retention of the customers. With the increasing pace of time, it has been identified that the quality of service is linked with the customer retention. As the customers tend to experience an improved service, their level of expectation also increases. According to the study of Abdul-Fatawu (2016), the customer starts making mindful and unconscious judgments between different experiences with regards to the services that are regardless of the functioning sector.

The ability of the company for attracting and retaining the new customers is basically one of the core functions regardless of the offering of the products. This tends to capture the market and the attention of the customers. The customer retention refers to the likeness, identification, commitment, trusting, and enthusiasm of the consumers to indorse others, or have the intention to repurchase. As per the study conducted by Chuani (2017), customer retention points toward a sustainable commitment on the side of the customers and the company for maintaining the relationship.

The customer retention has been promoted as a flexible as well as a more reliable source of a higher level of performance. It offers a wide range of benefits that includes retention in employees, their higher level of satisfaction, provision of the quality service, sensitivity in terms of lower cost and price, constructive words of appreciation, greater number of shares in the market, higher rate of efficacy and quality assuring productivity. As per the research conducted by Daniel (2016), customer retention is considered to be the main goal in businesses that tend to practice the relationship with respect to marketing. Though the literal meaning and dimension of the customer retention may tend to vary among the industries and companies, there is a general focus of all the companies on the economic benefits which they can gain through customer retention.

As the tenure of customer grows, the purchasing volumes tend to grow, and the customers agitate while their replacement cost fall. In conclusion to this, the already engaged customers tend to pay a higher cost than the newly developed customers. Haruna (2015) has stated in his research that the grabbing cost the attention of a new consumer is five times more than the cost of keeping the previously engaged customer satisfied. All this requires potential efforts for inducing those customers who are satisfied with switching away from the existing suppliers. Customer retention can be done in two ways that are by moulding the high switching barriers or by delivering a better quality to keep customers satisfied.

Overview of Banking Industry of Pakistan

The banking sector of Pakistan includes approximately 31 banks, from which, there are five banks that are based in the public sector while the foreign banks are four in number. According to the study conducted by Michaels (2017), the local banks in the country are about 22 which are privately operating. In Pakistan, there are six banks that are the biggest contributors to the economy and have the major portion of the assets of the banking sector. To be more particular, the deposits which such banks make up are more than 57 percent while the rate of giving advances ranges up to 53 percent in the economy. These banks include, Habib Bank Limited (HBL), National Bank Limited (NBL), United Bank Limited (UBL), MCB Bank Limited, Allied Bank Limited (ABL) and Bank Alfalah Limited.

The banking sector industry is controlled by the State Bank of Pakistan (SBP), that administers the national banks under the domain of its prudential regulations which are known as PR in the language of the banking sector. Also, the banks also obey the international standards of Basel III. In addition, this sector has a huge potential. According to research conducted by Abidi and Chandio and Soomro (2014), the number of the bank accounts make a contribution of 43 million approximately in a large populace of 195 million. The reasons of this great modification can be credited to the inadequate accessibility of the technology in Pakistan, the hatred or reluctance for the banks because of the religious and ethnic reasons and also, the countless size of the unaware population living in the rural areas.

The potential of the banking sector is day by day increasing with the high speed technology and mobile internets, the start of Islamic banking and the increased level of awareness with regards to the benefits of banking in Pakistan. With respect to the overall performance, Aftab (2012) has stated in his research that the banking sector of the country is progressing. From the year 2009 to 2016, the total number of assets has improved from PKR 6,516 billion to PKR 15,134 billion that has doubled over a span of 7 years. The deposits of the banks have risen up to PKR 11,092 billion from PKR 4,786 billion. Whereas, the lending ratio has increased up to PKR 5,025 billion from PKR 3,240 billion.

Since the year 2009, the rate of investments has been exponentially increasing after PKR 1,737 billion to PKR 7,625 billion in 2016 (Michaels, 2017). These changes took place in the time duration when the prudential regulation imposed great strictness for the banks that have been opposing in the industry. In the previous years, SBP has to be big enough so that the banks function well in the macroeconomic situations. According to the study conducted by Mirza, Berglan, and Khatoo (2016), in the year 2017, the performance of the banks was not so satisfactory because the interest rate had increased. It happened since there was a very big chunk of the securities of government that got developed in the period of June or July in 2016.

These were the reserves which the banks credited back in the year 2011-12 when the interest rates had an upward shift. As now the large chunk of these securities are mature and have left the market, it is predictable that the margins of net-interest in the banks will rapidly increase in the year 2017, whereas the NFI i.e. non-funded income will also have a downward shift due to reduced unrealised securities increases making many revenues than what is being accessible in the market (Shah and Khan, 2017). Nevertheless, the earnings will continue to be in check because, for the past years, many banks are clearing their balance sheets. Through the provision of the limited expenses, the future outlook of the banking sector will get stronger with the sharp increase in the rate of GDP.

Due to the low discount rates, the banks are now reverting back to their business of lending. These large chunks will be a means of a large source of funds for the market and this will let the business market expand more. Not only this, but it is also expected that a great deal of investments would be there due to the China-Pakistan Economic Corridor (CPEC) through which, the industry of infrastructure and development would grow more (Michaels, 2017). Though the lending business of the local banks in CPEC has limitations and is divided among HBL, UBL and Chinese banks, the impact of the mega infrastructure projects will provide ease to the banking sectors in the upcoming years.

Impact of Service Quality on Customer Retention

According to Zafar et al. (2012) the influence of the excellence of services on the consumer retention and loyalty of customer is significant and crucial to understanding in a growing economy like Pakistan. The element of consumer satisfaction is the most significant element in customer retention and loyalty. As the world is becoming modern, people are become more conscious about the quality of products and services and the banking system of Pakistan has developed more focused strategies to satisfy their customers’ building trust and loyalty.

Customer retention and service quality

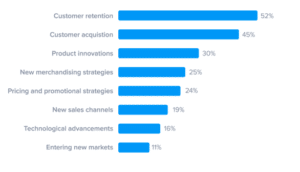

Hassan et al. (2013) highlighted that the most important aspect is the service value on retention of customers in the banking sector of Pakistan. The majority of the banks monitor and evaluate their customer retention through the excellence of their services on daily and monthly basis which ensures to maximise the loyalty, consumer satisfaction and improved customer retention. The figure below shows that consumer retention is the most important feature that drives the majority of the revenue of the banking sector in Pakistan. 52 percent revenue is generated from customer retention whereas customer acquisition and other factors come after customer retention in emerging more profit in the banking sector of Pakistan.

Figure 2 Factors affecting growth of bank

(Source: Chitra and Subashini, 2013)

The positive consumption experience safeguards the services and product quality. Whereas several customers who visit banks did not give a guarantee to revisit the bank, for this banks need to provide them effective services through which their loyalty level increase from the services of the bank.

Reliability and Customer Satisfaction

From the research of Sabir et al. (2014), it is illustrated that the connection among service excellence dimensions and customer retention was examined by through the lens of reliability. An important and constructive relationship among service reliability and customer retention was found that helps to boost the profit and increase the trust level of customers with the banks. It is observed that a positive association decree among consumer retention and service quality and bank performance are all directly and indirectly dependent on the reliability and dependency of customers and bank on each other. Moreover, Toor et al. (2016) discussed that the advancement of technology has increased the reliability of customer on banks through the online banking system and mobile bank by using apps on every location and everywhere conveniently which has become the most important and reliable source for all the customers of the bank. This also creates competition in the competitive market due to which the challenge of developing a more effective approach has been increased in this dynamic competitive world.

Service quality and customer loyalty

According to the research conducted by Khan and Fasih (2014), there has been a strong and effective affiliation among customer loyalty and service superiority that impacts on buyer retention. The level of customer retention in the banking sector increased by increasing customer loyalty which automatically increased by the services quality and attention provided by the banks. Whereas, in the competitive environment, the banking sector achieving the biggest challenge of maintaining the customer loyalty because in Pakistan, approximately all the services are similar in the banking sector and everyone provide those similar services with alternate names and procedures due to which it is most challenging for the Pakistan’s banking sector to maintain the customer loyalty. Moreover, the loyalty of customers has a potential impact on consumer retention which affects the profitability level of the bank.

Theoretical Framework

Resource-Based View

According to the study of Barney (2012), the Resource-Based View pursues to define the competitive advantage of an organisation and its performance according to the resources that customers need to fulfil their requirements. The resource-based view theory was designed to evaluate the resource control that are valuable, rare and non-imitable and could not be replaced. This theory suggested that the company need to analyse the need for resources of their customers by evaluating and taking feedback from them and analysing the competitive source to fulfil the demanded resources. Moreover, Ahmed et al. (2017) highlighted while implementing resource-based view theory to analyse the effect of facility quality on the customer retention in the banking sector of Pakistan came to know that the banks provide service to their customer according to the resources that their consumers needed to sustain their position in the competitive market. The capabilities and resources in banking are the main and important focus because it defines the performance of the organisation by analysing the customer retention rate through service quality. To rise a competitive edge in the banking sector, they must not have static resources; it should be unique from other banks so that more and more customers can easily retain and it could be the most reliable approach for the banking sector of Pakistan.

SERVQUAL Model

Ali and Raza (2017) highlighted that the instrument of multi-dimension research is SERVQUAL, which was designed to capture and evaluate the opportunities of consumers and their observations of the services provided by the organisation through five proportions of service quality. The model of SERVQUAL was recognised on the paradigm of expectancy disconfirmation, which defined and elaborated the service quality according to consumer satisfaction and it leads to customer retention with the organisation. Moreover, Ahmed et al. (2017) discussed that in the banking sector, the pressure has been increased to determine and establish services that attract the customers and majorly focused on the on-going performance and improvement of banks and their consumers. Providing resources and financial access to customers with an effective strategy can lead to customer satisfaction. Through the SERVQUAL model, the banking sector easily measured and set approaches that are significant for consumer satisfaction and this model also explains that customer satisfaction reduced the gap of customer retention by providing service quality by banks. The SERVQUAL is the most successful popular for the quality services that mostly implemented in the majority of the banks of Pakistan.

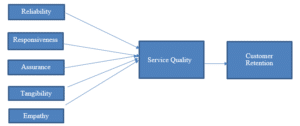

Conceptual Framework

In this chapter, some of the factors have been identified that have a direct or indirect influence on the service quality. In the banking sector, these indicators have a vital role in the determination of the excellence of the services. The performance of the banks is not based on the medium that it is using for the deliverance of services whether manual or online, but they are more inclined on the reliable services that ensure quality and meet up their level of satisfaction. The factor of reliability is the capability of delivering services as per the commitment. The point of attraction for the customers is undoubtedly the factor of trust.

Moreover, the customers remain satisfied if they get a timely response to whatever their concerns are, with respect to the services delivery. Giving assurance to the customers through the insurance that the company is highly concerned about safeguarding their trust is the responsible attitude that tends to increase the level of quality services. The provision of the tangible equipment and other resources is very important in order to have better services. Furthermore, the element of empathy builds up a connection between the consultant and the customers which tend to develop a long-term relationship. Overall, having these factors ensures that the better services excellence is to be provided to the customers that meet their satisfaction level.

Summary

In a nutshell, this chapter is comprehensively designed to discuss and estimate the influence of the service quality on the consumer retention. This topic is discussed in the background of the banking sectors of Pakistan. The quality of services is the delivery system of the services with a positive result by the customer retention while ensuring that the profits rise, and a constructive image is developed in the rivalry market. Though, the quality of services is directly associated with the customer retention and the service quality which is supposed by the customers. Consumer retention is significant for getting success in service businesses just like banks. The quality of service is a significant aspect in the retention of the customers.

With the increasing time period, it is identified that the service quality is interconnected with the customer retention. As the customers tend to experience an improved service, their level of expectation also rises. Currently, in Pakistan, there is the trend of e-banking which is the most preferable due to its speediness and easy services. The majority of the customers fulfil their requirements through the mobile application of their specific bank in the country. This has not only increased the service quality but also the customer retention that has reduced the number of visits and other formalities. The service quality is based on some of the significant factors that are reliability, responsiveness, assurance, tangibles, and empathy. These indicators have a vital role in the determination of the quality of the services.

CHAPTER 3: METHODOLOGY

Introduction to the Chapter

Methodology used in this study is being discussed in this chapter. To make the research substantial, the selection of methodology is highly essential to avert the research in a right direction which is suitable to the focus of the research and is also convenient for the researcher. In this chapter, the researcher has discussed the major aspects of methodology which are used to obtain distinguishable and significant outcomes. Moreover, the application of research approach and research philosophy are also the important part of the methodology. Design of the research is also been considered to identify the nature of the research that whether it is based on qualitative or quantitative grounds. Other fundamental details are also discussed in this section such as types of investigation, method of sampling and sample size which are selected accordingly to amplify the accuracy of the results. Lastly, data analysis, ethical guidelines and research limitation faced during the conduction of this research has been discussed.

Research Philosophy

This aspect is highly vital to define the trajectory in which the research is going to be conducted. It defines the process of how the data for the research will be gathered, analysed and utilized in accordance to the possible outcomes. It involves two factors epistemology and doxology. Epistemology defines something which is known to be true. On the other hand, doxology refers to something which is believed to be true. These two aspects covers multiple research philosophies regarding research approach. The research philosophy is further divided into multiple types including interpretivism, pragmatism and positivism (Sekaran and Bougie, 2016). According to the past literature, majorly used philosophies are interpretivism and positivism. Interpretivism allows the researcher to interpret the components of the subject and make sure that it is conducted organically. This philosophy is mostly used for qualitative analysis. In contrast to interpretivism, positivism involves the approach which depend on the scientific evidence of the subject in the form of experiments (Hovorka and Lee, 2010). It allows the researcher to understand the study in an objective manner.

Mixed method approach is being used in this study, this is why the researcher has selected the pragmatism research philosophy to carry out this study where the researcher has included the both quantitative and qualitative data to identify study the factual and subjective information in comparison.

Research Approach

To practice the appropriate way of research conduction, research approach is also very fundamental. Research approach have two main types which are vastly used by the researchers, such as inductive and deductive approach. Inductive approaches are the one where researcher tends to utilize the material provided from past studies and does not develop their own theory. While deductive approach means the approach in which researcher proposes their own hypothesis and does not limit the research to the already introduced theories and researches (Gottfredson and Aguinis, 2017). The selection of the research approach is based on its nature whether it is qualitative or quantitative.

Researcher has applied the deductive research approach in this study to obtain the estimated conclusions. The reason to use this approach is that the study has analysed the qualitative and quantitative data together to investigate the previously developed hypothesis which were tested in this study.

Design of Research

Design of research is a core element of research study in which methods and logical reasoning to solve a research problem are provided. The two generally used research designs are quantitative and qualitative designs. Qualitative research design refers to the data analysed and collected on the basis of its quality and content (Maxwell, 2012). The data in qualitative design is non-numeric because it is detailed. It usually consist the data collected from participants through interviews or questionnaire. Whereas, the researcher opt for quantitative design when the data is numeric because in quantitative design data is mostly consist of quantifiable and numeric figures.

The nature of the data for this study is mixed, thus the researcher have selected the quantitative and qualitative data together. The data used for this research consists of numeric figures and quantitative and qualitative data information being taken through the interviews.

Types of Investigation

Research investigation methods helps in monitoring the methods of the research which have been used to execute the study. According to the previous studies, there are three types of investigation which are mainly used namely as explanatory, exploratory and descriptive investigations. Explanatory research investigation is the one focusing on cause-effect inter-relationship, and discuss the relationship between multiple variables used in the past studies, journals and articles and also called the casual investigation (Barsalou, 2016). In contrast, exploratory investigation researcher tends to opt for the subject which is not discussed in detailed manner in the past studies and it could also be a totally new proposition which was not considered previously. Descriptive investigation is the one where all the aspects of the study is thoroughly discussed in a suitable manner.

This research is revolving around the cause and effects of the variables that are under study, this is why researcher has selected the explanatory research investigation method. However, these are the factors which have been studied before but the study is using all of them together to investigate the selected topic of the research.

Methods of Data Collection

Method for collection of data for the research is selected in accordance to the accuracy of results and objectives of the research (Cooper, 2016). This is also the same as sampling method and sampling technique. In quantitative research design, to attain the appropriate interpretation of data, the data must be sufficient and significant. Generally, two major methods for the collection of data are being used by researchers to carry out the study that are secondary and primary. The raw and direct methods for the collection of data come under the category of primary methods of data collection. While, the data used in secondary data collection method is from past literature, journals and studies.

This research is based on primarily collected data by the research with the help of surveys and interviews. The researcher has implemented the primary data collection method for this kind of study.

Sampling Method

Mainly, two major methods of data sampling are probability non-probability which has been adopted by the researchers according to the past studies (Uprichard, 2013). Probability sampling methods refers to the one where all the participants of the study have equal number of chances. Whereas, the number of chances given to the participants are not equivalent in the non-probability data method of sampling. Moreover, the probability method for sampling is divided into stratified and simple random data sampling techniques. In stratified data sampling techniques, the data is categorized in multiple sub group which was collected by the researcher from the large group of people in comparison to the simple random data collection technique which is unbiased.

Due to the realistic nature of non-probability data collection technique, it is most commonly used sampling method by the researchers. It is also divided into three kinds namely as convenience, non-convenience and snowball data sampling methods. As it is somehow indicates by the name of it, the convenience methods allows the researcher to conduct the study according to their convenience and accessibility. On the contrary, the snowball sampling technique is the one where the data is transferred between participants of the research. As the study required the researcher to collect the primary data due which it was necessary that the researcher should collect the data himself. Therefore, in this research, the conductor has preferred the non-probability and convenience data sampling techniques to prioritize their availability and accessibility. For interviews, the snowball sampling is selected

Sampling Size

When it comes to select the sample size of this study, it is necessary that the sample should be sufficient enough to represent the population which should be targeted by the study. Researcher has focused the commercial banks of Pakistan to investigate their service standards and the impact they are creating through their services. Therefore, it becomes clear that the sample should be large, as the population of this study includes all the commercial banks of Pakistan. For that particular reason, qualitative in being collected from 5 managers of commercial banks. However, the quantitative data is being collected from 150 customers of the banks to know their response regarding the service of the banks they are providing to them.

Data Analysis

This section of the study is highly crucial in relation to the conclusion of the study because it analyses the data collected to carry out the research whether it is primary or secondary (Smith, 2015). It is adopted in consideration of the data sampling method. The data utilized in quantitative researches are mostly analysed by the statistical and mathematical methods. The suitability of selection of the variables, dependents and covariates is vital for this part of the research. There are multiple statistical tools available for this purpose which is used to perform the analysis of the data including regression, correlation, ANOVA and etc. To maintain the substantiality of the data and objectives the data should be assessed in appropriate manner. The commonly used software for data analysis are SPSS and MS Excel.

In this study, the researcher used SPSS to apply the relevant tests over the collected data. However, the quantitative data has been analysed with the help of thematic analysis. While focusing the tests of the quantitative data, researcher decided to apply the regression and correlation analysis considering their relevancy to the study. In addition to that, frequency analysis has also been used in this study to analyse the quantitative data in detail.

Sampling Strategy

Sampling techniques are defined as identifying a sub-set of population that can be used in research process to represent entire population. The sample members are involved in data collection process for empirical data, the analysis and results of which are considered to be applicable on total population. General categories of sampling techniques are probability and non-probability sampling techniques (Brannen, 2017). The basic difference between probability and non-probability sampling techniques is that the former requires that the probability to participate and get recruited is distributed equally in the entire population while the former is free of any such restrictions. The main benefit of probability sampling techniques is higher reliability while the main limitation is that the researcher must have access to complete target population (Eriksson and Kovalainen, 2015). Since the target population in this study is marketing professionals in the UK, therefore it is a huge and the researcher did not have adequate means and channels to access all professionals in the UK. Hence probability sampling techniques were not feasible in this study (Walliman, 2015).

The sampling in this study was done using the convenience sampling technique. The convenience sampling can be used to access population members in the nearest vicinity and as per own convenience of researcher (Taylor, Bogdan, and DeVault, 2015).

The sampling process for questionnaire participants began with interacting with marketing professionals using social media channels and the researcher asked them to provide email addresses. The researcher sent blank questionnaire, blank consent form and research background in MS Word format to those participants who agreed to participate in the study. The researcher sent 156 emails and in response 100 complete questionnaire with signed consent forms were gathered. The data collection process was stopped at 100 sample size as it is an adequate sample size for statistical analysis. The same technique and process was applied for interview participants. Each interview was conducted using one-to-one interviews through multimedia applications in the smartphone. All discussions were recorded and then transcripts were prepared using the MS Word format.

Data Analysis Techniques

The data analysis technique is defined as a process that converts raw data into meaningful results and inferences and conclusions are drawn from results. Therefore are different data analysis techniques for quantitative and qualitative data. In case of quantitative data, statistical techniques are used (Silverman, 2016). The statistical techniques are highly appreciated in research community as they provide results in the form of tables and graphs which makes it easier to understand and analyse the data and interpret easily. However, statistical analysis cannot be chosen for qualitative analysis and they provide limited inferences as compared to qualitative data (Bryman, 2016).

This study used three statistical techniques commonly used in social research processes. The frequency analysis, correlation technique, and regression model were used to understand and analyse the quantitative data and explore the impact of social media marketing on sports marketing within the context of Nike. The impact of each variable in the conceptual framework was gauged using these techniques. The results and interpretations are presented in the following chapter.

For qualitative data analysis technique, there are several techniques which include thematic analysis, grounded theory, and content analysis, among others. In this study, the researcher used thematic analysis. Thematic analysis is a technique that enables the researcher to choose a set of keywords and then search them in large pieces of text(s), such as interview transcripts and sort the most relevant data called the categories. Once the relevant data is collected, the researcher further refines the data and identify common patterns and similarities in different pieces. These similarities and patterns are termed themes (Brannen, 2017).

The same technique and process was applied in this study. Since the interview questions were formulated using keywords from objectives, therefore, the researcher used thematic analyses and used the same keywords for search for themes in the interview transcripts. The results of the thematic analysis are presented in the form of a narrative in following chapter.

Ethical Guidelines

It is the ethical responsibility of researcher to ensure the confidentiality regarding information assessed from the participant. This research has considered the information available in the past literature, and all the rightful authors of those studies are credited in this study. Researcher has also followed the guideline to avoid the occurrence of plagiarism in this study which is considered an international crime if found in any documentation.

Limitations

It has been studied that there are some of the limitations in every study, therefore it is necessary that the researcher should identify and explain all the limitation itself. However, if the limitations are not being defined by the researcher, it is probable that these limitations would be considered as the weaknesses of the study. In this study, the researcher was provided with the limited time in which the study should have been completed. In addition to that, the budget was also limited, due to which the researcher was unable to meet the customers in person in order to obtain their responses for quantitative data. However, both of the limitations resulted in a way that the researcher could not exceed the sample size of the study, therefore, it is possible that the future study studying the similar topic increasing the sample size would present the different results.

CHAPTER 4: RESULTS AND ANALYSIS

Introduction

The current chapter is aimed towards providing analysis on the data that has been gathered by the researcher. For presenting the data analysis, the interviews and survey questionnaires were carried out and its findings are presented in this chapter for better understanding the research phenomenon. The interviews have been carried out by the managers and survey questionnaire has been carried out by the customers of the commercial banking sector. The chapter is comprised of demographic analysis, correlation and regression along with the frequency analysis. The findings of the interviews have been presented in the form of thematic analysis and the chapter finally concludes with discussion on the objectives of the study.

Demographic Analysis

This section explains the demographic information of the research participants that has been selected for this study.

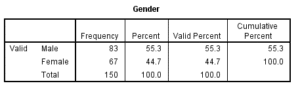

The first table explains the gender of the respondents and from the above figures, it can be asserted that out of 150 respondents, 83 were male and remaining 67 respondents were female depicting a majority of male respondents in the study.

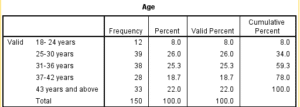

The table presented above explains the age of the respondents and from the table, it can be asserted that majority of the respondents were from the age group of 25-30 years. The second highest age group is estimated to be 31-36 years who have participated in this study.

Frequency Analysis

This section explains the results of the questionnaires which has been taken from the customers of the commercial banking sector of Pakistan.

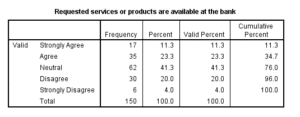

The first question which has been asked from the respondents of the study is associated with the fact that the customers are provided with the requested services or products and they are easily available at the bank or not. To this question, around 11% respondents positively responded to the question. However, a cumulative 34% of the respondents were strongly agree with the statement. The 41% of the participants remained neutral with the question statement and a total of 24% strongly negated with the question statement.

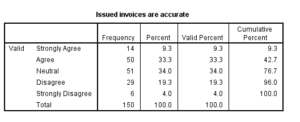

The second question which has been asked from the respondents of the study is related to the issued invoices are accurate. To this question, around 9.3% respondents positively responded to the question. However, a cumulative 42% of the respondents were strongly agreed with the statement. The 34% of the participants remained neutral with the question statement and a total of 23% strongly negated with the question statement. This implies that most of the respondents were in the favor of the statement that issued invoices are accurate.

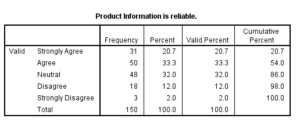

The following question which has been asked from the respondents of the study is associated with the fact that the customers are provided with the reliable information about the services or products. To this question, around 20% respondents positively responded to the question. However, a cumulative 54% of the respondents were strongly agreed with the statement. On the other hand, the 32% of the participants remained neutral with the question statement and a total of 14% strongly negated with the question statement.

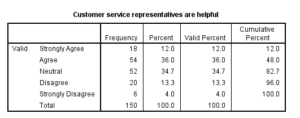

This question is related to the fact that whether the customer service representatives are helpful for the customers or not. To this question, around 12% respondents positively responded to the question. However, a cumulative 48% of the respondents were strongly agreed with the statement. The 34% of the participants remained neutral with the question statement and a total of 17% strongly negated with the question statement. This explains that a majority of the respondents were in the favor of the statement being asked.

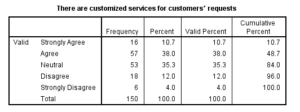

The first question which has been asked from the respondents of the study is associated with the fact that the customers are provided with the customized services on their request. From the findings of this question, around 10% respondents positively responded to the question. However, a cumulative 35% of the respondents were strongly agreed with the statement. The 41% of the participants remained neutral with the question statement and a total of 16% strongly negated with the question statement.

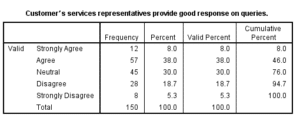

The first question which has been asked from the respondents of the study is associated with the fact that the customer’s services representatives provide good responses to the queries of the customers. To this question, around 8% respondents positively responded to the question. However, a cumulative 38% of the respondents were strongly agreed with the statement. The 30% of the participants remained neutral with the question statement and a total of 24% strongly negated with the question statement. The findings of this question imply that the respondents of the banks are provided with the timely resolution of their queries and hence the staff tends to be well-trained and quality conscious because they care about the customer’s wants and needs.

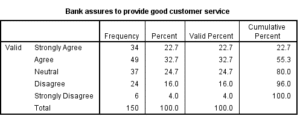

The following question pertains to the fact that the bank assures for the provision of good services to the customers in terms of commercial activities. To this question, around 22% respondents positively responded to the question. On the other hand, a cumulative 55% of the respondents were strongly agree with the statement that the bank provides good services to the customers. The 24% of the participants remained neutral with the question statement and a total of 20% strongly negated with the question statement.

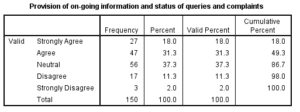

The question which has been asked from the respondents of the study is associated with the fact that there is a provision of on-going information and status of the complaints and queries. To this question, around 18% respondents positively responded to the question. However, a cumulative 49% of the respondents were strongly agreed with the statement. The 37% of the participants remained neutral with the question statement and a total of 13% strongly negated with the question statement.

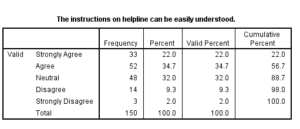

This question is asked about whether the instructions on helpline can be easily understood. To this question, around 22% marked strongly agree, 34% marked agree, 32% marked neutral. Furthermore, a total of 11% marked negative towards the statement being asked from the respondents. The analysis of the following statement implies that the instructions provided on the helpline can be easily understood by the customers which are quite necessary for the banks that their user-friendly services should always be assisting the customers.

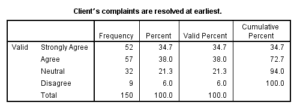

The question which has been asked from the respondents of the study is associated with the fact that the customer’s complaints are resolved at the earliest. To this question, around 34% respondents positively responded to the question. However, a cumulative 72% of the respondents were strongly agreed with the statement. Only 21% of the respondents were in the favor of a neutral response. Lastly, only 6% of the respondents marked negative to the student.

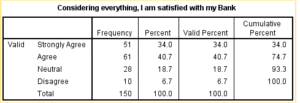

This question is related to the overall satisfaction of the customers with the banking services offered to them and level of their retention. To this question, around 34% respondents positively responded to the question. However, a cumulative 74% of the respondents were strongly agreed with the statement. Only 18% of the respondents remained neutral with the statement which implies that either they do not understand the question or does not want to answer. Lastly, only 6.7% of the respondents disagree with the statement.

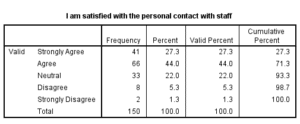

This question is related to the fact the customers are satisfied with the personal contact with the staff members of the banks. To this question, around 27% respondents positively responded to the question. Conversely, a cumulative 71% of the respondents were strongly agreed with the statement. Only 22% of the respondents remained neutral with the statement and finally, only 6% marked disagree in questionnaire regarding the fact that the customers are satisfied with the personal contact with staff.

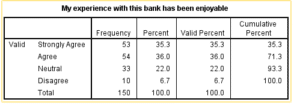

This question is related to the fact the customer experience with their respective banks is enjoyable. To this question, around 35% respondents positively responded to the question. However, a cumulative 71% of the respondents were strongly agreed with the statement. Only 22% of the respondents remained neutral with the statement which implies that either they do not understand the question or does not want to answer. Finally, only 6% marked disagree in questionnaire regarding experience.

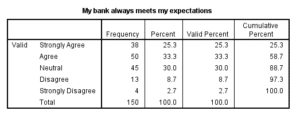

The question which has been asked from the respondents of the study is associated with the fact that the customers are provided with the services that could meet their expectations. To this question, around 25.3% respondents positively responded to the question. However, a cumulative 59% of the respondents were strongly agreed with the statement. Furthermore, the 30% of the participants remained neutral with the question statement and a total of 10% strongly negated with the question statement. This explains that majority of the customers were of the opinion that their bank meet their expectations.

Correlation Analysis

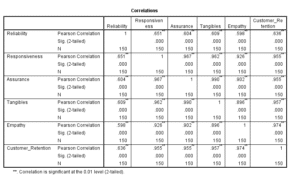

The main aim of the following study is focused on assessing the relationship between service qualities on the retention of the customers in the case of banking industry of Pakistan. For this purpose, a correlation analysis has been carried out for the purpose of assessing the relation between dependent and independent variables. In this case, a survey has been carried out so that the correlation analysis can be conducted. The table presented below explains the correlation between the variables of the study.

From the table presented above, it can be clearly observed that the results are significant. Based on this table, positive and strong association has been identified between reliability and customer retention as the estimated value for the correlation is .636 with .000 significance value. Similarly, the correlation between responsiveness, assurance and customer retention is estimated at 0.955 depicting a strong correlation. The factor of service quality i.e. tangibles is found to be at .957 correlated with the customer retention. Moreover, the relation between empathy and customer retention is estimated at .974.

Regression Analysis

This section deals with the explanation of regression analysis where the identification of the impact of independent variable with the dependent variable is constructed on the study. The regression analysis is regarded as the most useful statistical test for evaluating the relation between the two variables In the context of this study, the results of regression analysis are presented below,

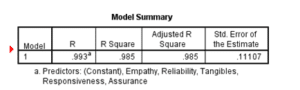

From the table of the model summary presented above, it can be assessed that the value of R-square is .0985, which means that variance in all the independent variables of this study including, responsiveness, tangibility, empathy and customer retention are explaining 98.5% variations on the variable for the actual usage. Considering the value assessed on the R-square, a fitness of the model can be observed in this research.

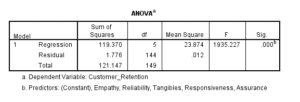

The table presented above explains the ANOVA of the study which explains that the empathy, reliability, assurance and other related factors of the service quality are the predictors of the customer retention. Moreover, the significance value is also estimated at .000 explaining that there is strong prediction of both dependent and independent variable relation.

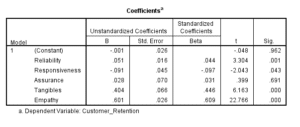

The coefficient table mainly explains the significance of the variables which are taken into consideration as independent variable. It can be observed that only assurance and responsiveness are found to be not significant, whereas, rest of the variables are significant for the customer retention.

Thematic Analysis

Significance of Service Quality and Its Trend in Banking Sector

Service quality is known as the delivery system of service for best output which also helps in retaining the customer. It plays a major role in rising profits and developing a positive image in the competitive market. It is investigated that service quality is directly associated with customer retention and service quality has been perceived by the customers (Kaushik, 2013). Service quality is regarded to be important in every aspect of the businesses as from the respondents it is analysed that:

“I consider service quality to be most important aspect in the business as it helps in satisfying the needs as well as demands. People consider is very important as it helps the organisation in meeting the expectations of the customers as well as it also help in competition with the competitors as well as environmental actors, nature of services and the factors which affects the organisation internally.”

From the previous researches it is analysed that the improvement in service quality not only improves the satisfaction level of the customers but also helps in increasing the streams of revenue which is very important for the organisation as well as the employees working in it (Urban, 2013). As per the response of another respondent:

“The main benefit which I consider through the service quality is that it helps in enhancing the revenues. This is possible by retaining the higher percentage of the customers that already exists as well as it attracts several customers by positive words and the rates of existing customers are also increased with the help of this. This is my point of view but other contradicts from my point of view. There are people that consider service quality to be important as it determines the satisfaction of customers. The consider quality as a prime thing which affects the success and failure of the business. Most of the people associates quality with the consistency but the main thing which should be considered is that the products are mainly developed as per the quality standards of the company.”